Why Your Lending Business Needs APIs: A Complete Guide to Lending API Integration

The 'Application' in APIs refers to specialized software that supports a variety of tasks on digital devices. In the credit industry, applications vary in scope, including loan initiation platforms, CRM tools, credit evaluation systems, or banking apps on handhelds.

APIs integrate these diverse applications, serving as a vital link and enabler of data transfer. A prime example would be a loan generation system that liaises with a credit bureau’s scoring system through a loan origination API. The result? A simplified procedure, courtesy of direct credit score transfers to their systems.

APIs: Gaps and Bridges

Following the alphabetical nomenclature, 'B' postulates for 'Bridge'. Acting as bridges, APIs facilitate interactions and transfer of information between disparate software applications, by standardizing their communication rules.

With APIs as an active intermediary, discrepancies among various systems incorporated in loan inception can be significantly reduced. A loan origination API eases connectivity between a lender's software and a third-party confirmation service. Consequently, income and employment data verification can be carried out directly within the system, bypassing the need for separate checks.

Communication Catalyzer: APIs

"C" endorsing 'Communication' in APIs, aids information exchange between differing software. They do so by defining a sequence of directions or invocations, that one application can forward to another.

In the loaning sector, APIs accelerate communication between systems engaged in loan inception. For example, a loan-seeking customer sends a request through a lender's mobile app. The requisition is then carried forward, using an API, to the lender's primary software. Subsequently, a separate API is employed to procure a credit score from a credit agency, while another is utilized for verifying the borrower's financial and employment information. Such synergized information exchange greatly accelerates loan initiation.

APIs: Reshaping the Lending Environment

In reinventing the loaning arena, APIs have given lenders the tools to automate loan inception and enhance both speed and accuracy. Synchronizing various platforms and services through APIs allows lenders to refine and customize the client experience.

Moreover, APIs have paved the way for groundbreaking developments in the sector, providing a uniform platform for application interaction, which facilitates an easier assimilation of new technologies. The use of artificial intelligence and machine learning within the loan inception process is a fitting illustration of this. With APIs, lenders can seamlessly integrate these advanced technologies into their systems.

The impact of digital innovation is evident across various sectors and the finance industry is no exception. APIs or Application Programming Interfaces drive significant portion of this change, particularly in the lending sector. These mechanisms facilitate varied software applications to engage in dialogue, fostering streamlined operations in lending businesses.

APIs serve as communication channels between a loan origination system of a lending entity and other key stakeholders such as credit bureaus and banking institutions. With APIs, all involved parties can exchange information in real-time, which aids the lending institution in making prompt, informed decisions regarding loan authorizations.

APIs can also enhance customer satisfaction in lending trade. Today's borrowers value swift, effortless, and transparent procedures and API implementations can satisfy these expectations. By integrating various third-party applications with the lender's platform via API, the lender can grant borrowers the ability to apply for loans, track loan progress, and manage repayments, all within a single system.

The integration of APIs in lending operations doesn't only end with ameliorating customer experience: It also optimizes operational efficiency. Automation of multiple procedures with the aid of APIs reduces the need for manual interventions, leading to fewer mistakes and time savings. APIs specific for loan origination can automate the complete loan creation process, from application receipt to underwriting and final sign-off, ensuring both the speed and accuracy of the task.

Apart from these benefits, APIs at the same time ignite innovation within the lending field, offering a structure for inclusion of multiple systems and applications. Certain lending institutions exploit APIs to propose a "loan as a service" concept, sharing their loan origination processes with other trades through an API. This provision permits those businesses to propose loans to their clientele devoid of creating their independent lending structure.

APIs also contribute to adhering to important regulatory compliance norms. Lending institutions can use APIs to link their systems with regulatory databases to rapidly and precisely validate customer credentials, maintaining conformance with Anti-Money Laundering (AML) and Know Your Customer (KYC) legislation. Hence, the influence of APIs on the lending business underscores their importance in streamlining procedures, uplifting customer experience, inducing innovation, and ensuring regulatory conformity.

Principal Features of Loan Initiation APIs

Loan initiation APIs, essentially software intermediaries, facilitate interaction among distinct software modules. They supply a regulatory framework for formulating applications and software. In terms of lending, this results in the computerization of the loan issuing process, from the initiation of the application to the release of funds.

Main features of the loan initiation API encapsulate:

- Processing Applications: The API is receptive to loan requests from an array of sources, verifies the shared information, and maneuvers the application accordingly.

- Underwriting Services: The API commercializes the underwriting operation, including credit dilation, evaluation of risk, and credit cost.

- Credit Approval: Depending on the outcomes of underwriting, the API reaches a decision regarding the loan, either consenting or declining the application.

- Allocation of Loan: If the application for a loan achieves approval, the API puts in motion the allocation of funds to the borrower's account.

Composition of Loan Initiation APIs

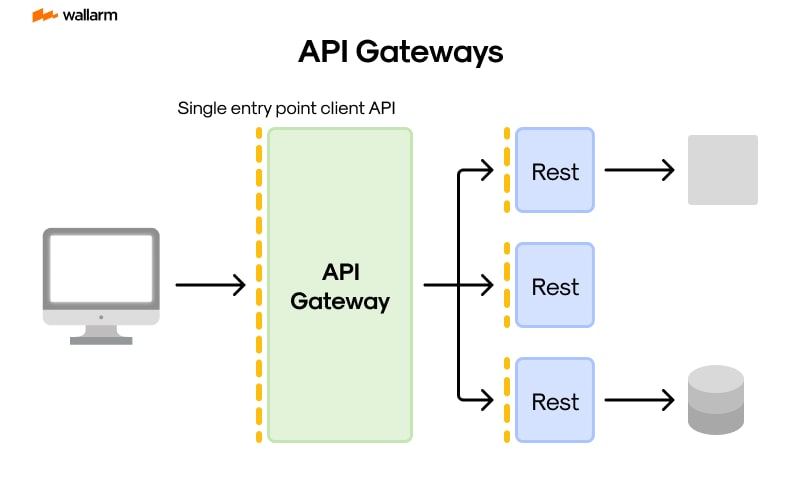

Generally, loan initiation APIs adopt the RESTful design blueprint, signifying Representational State Transfer. This design paradigm rests on specific constraints. When implemented together, these constraints facilitate the creation of APIs with coveted attributes such as performance efficiency, scalability, ease, modifiability, visibility, transferability, and dependability.

Here is the basic diagram illustrating the RESTful loan initiation API architecture:

This blueprint is composed of:

- The End-User could be a mobile app, a web application, or any additional software requiring interaction with the lending system.

- The API serves as the go-between, facilitating dialogue between the end-user and the data repository. The API discloses URLs to the user to perform various operations, such as submitting a loan request, checking the status of an application, etc.

- The Data Repository is the storage for all information related to the lending procedure. The API liaises with this repository to recoup or modify data as necessitated.

Loan Initiation API Workflow

The loan initiation API workflow essentially consists of the following steps:

- Request: This pertains to the end-user dispatching a request to the API. This could take the form of a GET request for data retrieval, a POST request for data submission, or a PUT/PATCH request for data modification.

- Processing: Here the API engages with the request. This could mean verifying the data from the request, performing computations, liaising with the data cemetery, etc.

- Response: Subsequently, the API responds to the end-user. This reply could contain the requested data, a verification of successful data submission, an error message, etc.

Consider this example of a loan initiation API process:

In this scenario, the end-user submits a loan request by dispatching a POST request to the API. The API maneuvers the request, verifies the data, actions underwriting, decides about the loan, and archives the application data in the data cemetery. Consequently, the API then replies to the end-user, indicating whether the application received approval or rejection.

Automation: Leveraging Efficiency

The complex infrastructure of loan origination APIs minimizes the manual labor involved in the initiation of loans. The intricate programming reduces the time taken to process loan applications, thus amplifying customer satisfaction and freeing up the workforce for other pursuits.

Instead of manpower physically checking income proofs and bank records - a process that could span hours or even days - loan origination APIs automate and quicken the verification, bringing it down to just a few minutes.

Better Decisions through Data Accumulation

These APIs also amplify the quality of decision-making in your firm by providing access to pertinent data. Information ranging from credit history and job stability of the borrower becomes readily accessible, paving the way for a thorough understanding of the borrower’s credibility.

Let’s consider a scenario where the API reveals a record of delayed payments on a prospective borrower's past loans. Equipped with such information, the decision could sway towards rejecting the loan application or granting it with a higher interest rate to offset potential risk.

Amplifying User Experience in the Digital Age

Modern consumers expect a seamless, effortless experience in this digitally-driven era. Loan origination APIs play a pivotal role here by enabling a smooth digital loan application platform.

Imagine allowing your customers to apply for a loan directly from your company's website or mobile application. The API consolidates necessary data such as credit scores and income details and swiftly provides feedback on the loan application. Such seamless user experience is central to attracting and retaining a faithful client base.

Reduction in Expenditure

Companies also benefit from cost savings by introducing automation to the loan initiation process with loan origination APIs. The elimination of extended manual checks and reduction in errors resulting from process automation significantly reduce costs.

Take the task of manual verification of employment status of a borrower. This task involves multiple calls, emails and significant working hours which can be automated by the loan origination API, leading to considerable savings in time and resources.

Adherence to Regulations

Lastly, loan origination APIs ensure regulatory compliance by predicting potential compliance issues. These systems ensure the borrower's income sufficiency for loan repayment, thus avoiding the implications of non-compliance such as hefty fines and penalties.

For example, an API can independently verify if a borrower's debt-to-income ratio adheres to lawful standards and highlight applications that violate these standards, requiring additional review.

Imperative Security Protocols for APIs in Loan Distribution

APIs are the backbone of loan distribution systems, calling for critical attention towards their security considering the confidential user data they manage. Tempting to cyber culprits, these APIs handle user-specific and transactional data with risks extending to data infringement, theft of identity and deceitful operations. Implementing rigorous security protocols is imperative for ensuring the safety of these APIs.

Here are a few critical protocols to enhance API security:

- Data Ciphering: Every bit of information flowing through the API network needs to be ciphered to render it unreadable even in case of interception.

- Verification: Access to APIs should be gated and every interaction should be upheld with a verification process. This may involve using API keys, tokens or employing other secured strategies.

- Access Control: Post verification, it is crucial to place controls for the degree of functionality each user is allowed. For instance, certain users may have clearance to look into loan details, but must not be entitled to approve or veto a loan.

- Activity Ledgers: Maintenance of detailed ledgers regarding all operations can facilitate tracking of any dubious occurrences and assist in a thorough examination during an instance of security breach.

- Request Regulation: Mechanisms to regulate the count of requests from a particular origin within a specific timeframe should be in place. This helps inhibit attempts to saturate the system with redundant requests.

API Gateways: The Shield for API Security

API gateways function as a primary defence for loan distribution APIs. They dictate the access to API and extent of functionality available to each user. Moreover, they enforce secure features such as data ciphering, request regulation and activity logging.

Adherence to Security Protocols and Norms

Loan distribution APIs must adhere to diverse security norms and codes, which include the PCI DSS, GDPR, and the CCPA. These codes impose stringent security procedures and stringent penalties in case of non-adherence.

Significance of Security Examination

Periodic security audits, which include penetration examination to identify and remedy potential vulnerabilities and protocol adherence checks, are vital for the solidity of loan distribution APIs. This ensures the APIs are abiding by the mandated security procedures and norms. The security examination acts as a proactive measure for maintaining the integrity of the data flow through the API network.

Businesses striving to maintain an edge in the dynamic world of financial transactions can revolutionize their lending operations by embracing the potent capabilities of loan inception APIs. These strategic tools present immense opportunities for operational transformation, exceptional client servicing, and increased return on investment.

Harnessing the Potential of Advanced Automation

Loan inception APIs are programmed to automate lending processes, significantly accelerating the journey from a loan request to its sanctioning. The automated system diminishes human glitches, offering a highly efficient and precise modus operandi.

Take an example of data collection. Conventionally, data entries are labor-intensively registered into systems. With loan inception APIs, data can be fetched automatically from several resources, such as credit rating agencies, and instantaneously placed into the loan inception system. Thus, creating an environment of swift operations and ensured accuracy.

Sculpting an Impressive User Journey

The technologically savvy customer base of the current times anticipates expedited, hassle-free services. Loan origination APIs can achieve exciting customer interactions by offering prompt updates and speedy loan processing.

Consider how customers can forward their loan applications digitally and relish an immediate tentative approval according to the data gathered by the API. This swift response eliminates extensive waiting periods, thereby enhancing the user's association with the business.

Orchestrating Efficient Operations

Loan inception APIs present an opportunity to synchronize multiple systems. A single data entry or update becomes available across all integrated platforms, emulating manual data replication's tedious requirement.

To put it in context, if a client modifies their contact details on one platform, the API permits an automatic update of this information across all associated systems. This leads to consistency and correctness of the data, which are fundamental for an efficient lending business.

Expanding Profit Margins

The automation and consolidation capabilities offered by loan origination APIs significantly curtail operational expenses. The resultant savings can be directed towards swelling profit margins.

Moreover, these APIs can improve the client's experience with your business, encouraging customer loyalty and attracting potential clients, contributing to your business's profitability.

Pioneering Loan Origination APIs

The journey to integrate loan origination APIs should start with:

- Needs Assessment: Pinpointing your business requirements is instrumental in selecting an API that matches these needs.

- Right API Selection: Several loan inception APIs are available, each offering unique features and capacities. It is essential to opt for one that synchronizes with your business aspirations.

- API Testing: It is recommended to validate the API's functionalities through testing before fully integrating it into your operations, to address any potential issues.

- Staff Training: The successful incorporation of a new API necessitates imparting adequate training to your personnel to use it effectively.

- Performance Monitoring: Post-integration, vigilantly observe the API's functionality and tweak it as needed to maximize its benefits.

Analyzing Risks: The Starting Point

The loan granting API process begins with an all-encompassing risk scrutiny. A variety of factors such as the potential borrower's lending history, duration of employment, level of earnings, and the ratio of debts to income are thoroughly assessed to evaluate the likelihood of financial mishaps. Using complex computational models, the API breaks down this data to draw up a risk snapshot for the would-be creditor, determining the feasibility of forwarding a loan.

Accumulating Application Details: Gather and Verify Phase

Following risk evaluation, the API delves into collecting loan application specifics. Exhaustive data, varying from personal particulars of the prospective debtor such as financial circumstances to minute aspects of the desired loan, are collated. The API's foundation is its automation, which automatically completes fields based on the prior risk assessment information, streamlining the paperwork for the applicant.

Undergoing the Underwriting: Pivotal Point

There's no doubt that underwriting holds a key position in the loan inception process. Here, the loan granting API exploits the previously accrued data from both the risk examination and the loan application to decide the loan's fate.

Demonstrating its complexity, the API utilizes sophisticated computational models to calibrate the potential risk and anticipated returns of the loan. Considering elements such as the applicant's risk snapshot, loan sum, and interest standards, it enables the final verdict on the loan endorsement.

Greenlighting the Loan: Implementation Phase

Subsequent to thorough underwriting, the loan granting API reaches its ultimate step of loan greenlighting. Should the weighed risk be acceptable, approval is given. As a result, the API changes course to commence the loan disbursement process.

Boasting efficiency, the API has the capability to auto-draft loan documentation, plan fund allocations, and deliver timely notifications to both the lender and applicant.

Unpacking the Loan Procedure

At a macro-level, API-facilitated loan inception unfolds linearly:

- Risk Scrutiny: The API closely probes the risk associated with a potential debtor.

- Gathering Application Data: The API methodically gathers in-depth data from the applicant.

- Loan Underwriting: The decisive power rests with the API, it uses the collated data to make the ultimate decision on the loan.

- Loan Greenlighting: Post loan's endorsement, the API takes the front seat in launching the loan disbursement proceedings.

The complete procedure is designed for high efficacy and productivity, enabling a smooth lending process for both parties involved. APIs used in this context have the potential to greatly aid money lenders in improving their lending decisions, reducing financial hazards, and elevating the overall lending experience.

Utilizing APIs: A Key Component in Adhering to Regulatory Rules

Employing loan origination APIs has impressive influence in maintaining regulatory compliance by leveraging process automation capabilities, as mandated by lending-related rules. Below we delve deeper into their functions:

- Ensuring Data Precision: APIs allow for instantaneous data exchange, which keeps an check on the data's accuracy—an essential demand for regulatory rule-adherent record-keeping.

- Masterful Documentation: The utilization of APIs records and logs all the activities during the loan initiation process, culminating in a thorough audit report— a must-have as per regulatory compliance rules.

- Implementing Risk Management Tactics: The harmony between APIs and risk management tools enables loan providers to identify and reduce risks, fulfilling the regulatory stipulations to maintain risk within defined rules.

APIs: A Path Through Compliance Hurdles

APIs present an answer to the quandary experienced by loan lenders due to stringent regulatory compliance:

- Adapting with Regulatory Revisions: Regulatory amendments are par for the course in the loan industry. However, APIs utilize their inherent flexibility and expandability to adapt swiftly to these revisions, hence closing any gaps in compliance.

- Enhancing Data Protection Standards: To adhere to compliance laws, robust data protection practices are essential. APIs, equipped with advanced security measures, can provide the necessary support to loan lenders in meeting this requirement.

- Boosting Operational Openness: By keeping a detailed log of all transactions taking place, APIs ensure that lenders meet the obligatory operational transparency levels.

How APIs Influence Compliance Management: A theoretical Illustration

Take for instance, LoanFlow, an imaginary lending entity grappling with manual procedures and obsolete systems. Incorporating a loan origination API revolutionized their operations: not only was the compliance-related functionality automated, but discrepancies were eliminated, enabling the generation of highly detailed audit reports. This improved their operational output to comply with strict regulatory specifications.

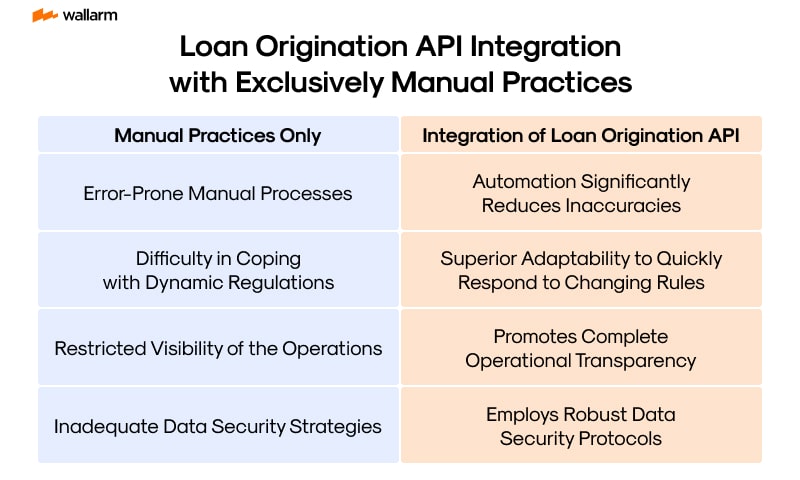

Contrasting Loan Origination API Integration with Exclusively Manual Practices

AI and ML Transforming Loan Origination

The lending industry is on the brink of a transformation driven by AI and ML, intricately woven into Loan Origination APIs. AI-driven automation introduces greater precision and swiftness, performing tasks such as verifying applicant data against diverse databases. This upgrade not only accelerates operations but mitigates fraudulent activity possibilities.

ML extrapolates meaningful patterns from an extensive dataset, such as determining a borrower's potential default likelihood based on past records. Lenders, equipped with these insights, stand better chances of averting unviable lending scenarios.

Blockchain In Loan Origination – A Security Revolution

Imagine integrating blockchain's inalterable nature into Loan Origination APIs. The appeal lies in storing each transaction on an unmodifiable, distributed ledger, guarding the loan initiation process's safety and transparency.

Borrowers' data could find a safe haven within the blockchain, maintaining its sanctity. Employing smart contracts introduces automation in loan agreement formalities, lessening manual involvement and fostering efficiency.

Instant Risk Assessment – A Future with APIs

Loan Origination APIs might soon transform risk assessment from a tedious undertaking to a swift one. Traditional approaches, time-consuming, involve assessing several factors like the borrower's income, credit history, and more. Technological progress promises instant risk assessment capabilities within APIs, offering lenders immediate intel about a borrower's credit standing.

Integration of diverse data platforms, encompassing credit bureaus, banking institutions, even social networking sites, fuels real-time risk assessment. APIs, armed with this real-time data, deliver an extensive and precise risk profile of the potential borrower.

Advancing Customer Interaction with Loan Origination APIs

APIs within lending might soon elevate the borrowing experience, owing to their customization potential. They could deliver loan propositions tailor-made to a borrower's financial profile, potentially bumping up customer satisfaction levels along with loan closure rates.

Real-time updates regarding loan applications status offer relief from uncertainty while escalating transparency. Moreover, APIs simplify the loan agreement process, reducing paperwork and making the process friendlier for borrowers.

Tactical Mapping of Business Requirements

Without doubt, clearly demarcating your corporate requisites should be your initial endeavor. What quandaries do you aim to obliterate? What aspirations motivate the integration of a loan initiation API? Comprehending these factors will assist in homing onto an API perfect for your corporate mission.

Making the Apt Loan Initiation API Selection

The market is saturated with a variety of loan initiation APIs, each offering unique traits and functionalities. APIs are engineered for various requirements: some are ideal for miniature-scale industries, others are suited for hefty corporate bodies. Some APIs come fully loaded with features, while others specialize in specific loaning processes. It's important to closely inspect, evaluate their capabilities, and eventually opt for the one tailored for your corporate requirements.

Strategizing the Execution Blueprint

Post pinpointing the appropriate API, the subsequent phase involves meticulously formulating your execution blueprint. Core elements like timeline stipulations, resource allocation, and establishing a dedicated project management crew need careful deliberation. Considering the inevitable hurdles and potential risks and designing an emergency protocol are paramount as well.

API Consolidation

The consolidation process signifies interfacing the API with your prevailing systems and platforms. Certain technical skills could be required, hence roping in a specialist might be advisable. Thorough configuration and testing of the API should be ensured before progression.

Personnel Training

To employ the new API effectively, personnel need to be well-versed with it. Comprehensive understanding of the features, software navigation, and troubleshooting common hiccups should be imparted. Thorough training and backing will naturally culminate in a seamless transition.

Continuous Monitoring and Assessments

Post API integration, it's imperative to continually assess its performance and operational effectiveness. This involves tracking pivotal metrics, interpreting user feedback, fine-tuning accordingly. Regular inspection and evaluation will aid in optimizing the API’s benefits and ensuring its long-standing success.

Elevating Security with Wallarm AASM

The concluding imperative phase involves safeguarding your API, facilitated by Wallarm API Attack Surface Management (AASM). Wallarm AASM is an independent detection service designed specifically for the API ecosystem. It aids in discovery of external hosts with their API, detecting absent WAF/WAAP solutions, unveiling vulnerabilities and taking measures against API Reveals.

With the facilitation of Wallarm AASM, the security of your loan initiation API is elevated, thus shielding your corporate environment from looming threats and susceptibilities. This product can be explored freely at https://www.wallarm.com/product/aasm-sign-up?internal_utm_source=whats.

The integration of a loan initiation API is certainly a significant stride towards the path of corporate modernization. Adhering to these consecutive phases, ensures a rewarding and successful implementation, enhancing operational effectiveness, refining client services and boosting revenue generation.

FAQ

References

Subscribe for the latest news

.png "AWS with Wallarm")