The complete guide PCI compliance

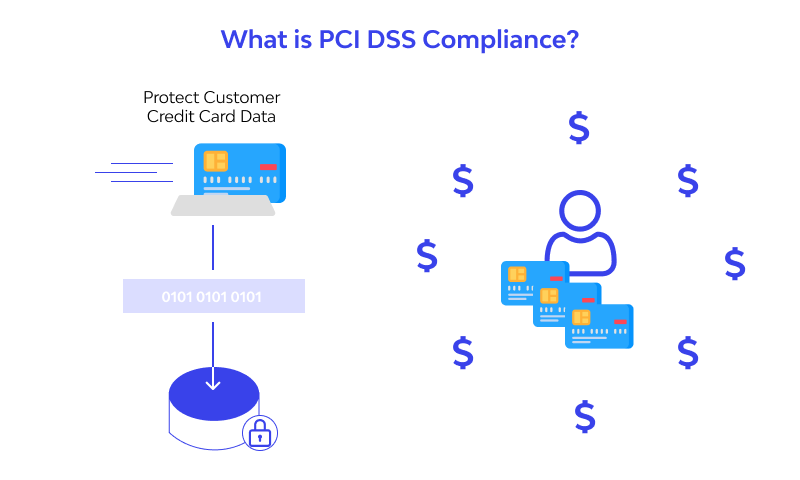

In this day and age, the web is everything. Our everyday lives, suppers, flights, schooling, etc, can be reserved or procured over the web. There perhaps a few situations that expect you to make installments to a site or merchant. When you input your card data into the site, exactly how secure is your information? PCI manages the security of credit and check cards utilized in the computerized space.

PCI DSS, otherwise called Payment Card Industry Data Security Standard, is characterized as the arrangement of prerequisites or rules that influence associations that handle card installments. This sounds like a clear idea. Indeed, it is. In any case, this straightforward idea can get dangerous if not appropriately overseen. Did you realize that PCI consistency can be an issue for associations who come up short on the right gear and apparatuses to do the necessary cycles?

In this article, we'll be investigating the rudiments of PCI Compliance, its prerequisites, and strategies that associations receive to guarantee PCI consistency and keep a solid network safety presence that wards off dangers. Before we start, observe that the place of PCI isn't simply to mark a container and pronounce you agreeable yet to ensure the data of the cardholder against any pernicious dangers.

What is PCI Compliance?

At the point when credit and check cards began to be utilized in the computerized space, it immediately turned out to be evident that there was a need to offer some type of insurance against misrepresentation. Vendors and sites are liable for handling installments needed to shield the information likewise that they would get actual money.

The issue during the previous years was that network safety specialists realized that they needed to ensure this information however were uncertain of how to go about it. The top charge card organizations were especially worried about how to ensure this pivotal data. Thus, every one of them created singular security guidelines to ensure cardholders.

From the outset, the organizations concocted individual inner data security programs. The presentation of unified consistency standards guaranteed that these individual projects fitted under a solitary umbrella. PCI Compliance form 1.0 was presented in 2004.

The current rendition of the consistence necessities is 3.2.1, which was created in 2018. The expert on PCI consistency is the PCI Security Standards Council which was created in 2006. They are a worldwide association that says precisely how organizations ought to secure credit cardholders in this computerized age and time of new network protection dangers. Asides from ensuring the information of the credit cardholder and keeping it from getting under the control of programmers, PCI is additionally intended to help groups and card guarantors limit the harm if a security penetration happens and prompts misfortune.

As indicated by the Verizon 2018 Payment Security Report, the PCI DSS is currently known as a demonstrated and solid system for installment security associations with various advantages for the association asides from the only assurance of card installment information. A review of Verizon's PCI clients showed that practically half (for example 49%) were guaranteeing consistency with PCI DSS guidelines to meet different necessities of information assurance guidelines, like the European Union (UN) General Data Protection Regulation.

PCI Compliance isn't an assurance of undeniable level security

The way that you have figured out how to get PCI agreeable isn't an assurance that your association can play out its capacity safely. The entire idea is something beyond checking that container. Yet, PCI consistency is an indication that you are prepared to make a stride the correct way. Ensure your inside security and consistency groups don't lose interest in making PCI consistency a piece of your general security program.

Attributable to the unpredictable idea of Compliance implementation when utilized worldwide, there are various PCI legends to observe. Significantly, you know how PCI consistency functions since it can assist your organization with getting an unmistakable image of potential dangers and the condition of your security framework.

Who needs PCI Compliance?

If your association is accountable for handling, putting away, or sending Mastercard information, you would have to embrace PCI DSS and be consistent with its guidelines.

Is there a punishment for neglecting to be PCI consistent?

It ought to be noticed that PCI isn't a law guideline. In any case, card guarantors should pay special mind to the security of their cardholders. This implies that guarantors would control their fines to merchants who are associated with any instances of information penetrates and have neglected to be agreeable with PCI rules. The acquirer and merchant benefit from the fine alongside different expenses, for example, card substitution costs, expanded charges for every exchange, etc. Fines for the most part range from $5,000 - $100,000 relying upon the terms of the arrangement between the acquirer and the seller.

Asides from the fines they pay for resistance, merchants may confront an on-location review and drop down a consistency level. This is the reason you need to illuminate your acquirer about your PCI consistency approaches so they can disclose to you how to shield yourself from any punishments.

Step by step guide to PCI Compliance

What is your Compliance level?

The truth of the matter is that a break in data of a private venture with a little computerized impression has lesser potential for making harm individuals from the public when contrasted with the penetrating of a huge retailer. Attributable to the various kinds of datasets that could be influenced by an information break, there are four (4) unique degrees of PCI Compliance which any association should fall into:

Level 1: Any merchant handling more than 6 million exchanges yearly across their channels or any seller that has endured an information break. Charge card organizations are permitted to overhaul any merchant to Level 1 as indicated by their watchfulness.

Requirements

- Document-level 1 on the spot examination – a yearly Report on Compliance (ROC) by a QSA or inside monitor at whatever point supported by an authority of the association

- Go through a quarterly association channel by Approved Scan Vendor (ASV).

- Complete the Attestation of Compliance (AOC) for on the spot assessments

Level 2: Any merchant that is handling between 1-6 million exchanges yearly on the entirety of their foundation.

Requirements

- Complete the yearly PCI DSS Self-Assessment Questionnaire (SAQ).

- Finish and get confirmation of a passing shortcoming quarterly range with an ASV

- Complete the AOC according to their SAQ game plan

- Submit SAQ, AOC, close by some other referenced documentation, to their acquirer

Level 3: Any merchant that is presently handling between 20,000 – 1 million exchanges each year.

Prerequisites

- Complete the yearly PCI DSS Self-Assessment Questionnaire (SAQ).

- Finish and get confirmation of a passing shortcoming quarterly range with an ASV

- Complete the AOC according to their SAQ game plan

- Submit SAQ, AOC, close by some other referenced documentation, to their acquirer

Level 4: Any merchant that is presently handling under 20,000 web-based business exchanges every year or any seller that is preparing up to 1 million exchanges each year.

Prerequisites

- Complete the yearly PCI DSS Self-Assessment Questionnaire (SAQ).

- Finish and get confirmation of a passing shortcoming quarterly range with an ASV

- Complete the AOC according to their SAQ game plan

- Submit SAQ, AOC, close by some other referenced documentation, to their acquirer

The positioning of the levels is very straightforward. The more exchanges you can deal with consistently, the higher the consistency level for the association. Nonetheless, you must know about how merchants can bounce from Level 4 to Level 2, ceaselessly at level 3. This abrupt bounce is subject to a business's development rate and several exchanges handled.

PCI DSS 3.2 Requirements and Security Standards

Make a safe organization and security framework

- Install and routinely keep a firewall set up that safeguards the information of the cardholder.

- Do not utilize merchant-provided defaults when searching for framework passwords and other security boundaries that you may require.

Secure data of the cardholder

- Secure any accessible and put away cardholder information.

- Code the transmission of cardholder information when managing public organizations.

Make and run a weakness of the board program.

- Secure the entirety of your frameworks against malware and consistently update any introduced hostile to infection programming or projects.

- Create and consistently keep up secure frameworks and applications that run for this reason.

Set up solid access control measures

- Restrict admittance to subtleties of the cardholder and ensure that such data is possibly made accessible when they need to know

- Identify and verify admittance to parts of the framework.

- Restrict any actual admittance to the information of the cardholder.

Consistently screen and test organizations

- Track and screen admittance to the organizations/assets of the cardholder information.

- Conduct ordinary tests for the frameworks and cycles that you have set up.

Keep an Information Security Policy

Maintain an arrangement tends to data security for various sorts of staff

Demonstrate PCI Compliance to one of our Auditors

To demonstrate that an association is agreeable includes four abbreviations which are QSA, ISA, ROC, and SAQ.

- Quality Security Assessor (QSA): QSAs are the individuals who are affirmed to perform PCI reviews on various associations. An association's yearly PCI QSA appraisal is the essential occasion that shows any proof of consistency is found.

- Internal Security Assessor: ISAs are the individuals who are responsible for consistency that handles consistent endeavors inside an association. They likewise have a PCI confirmation. These individuals are prepared to perform PCI self-appraisals.

- Report on Compliance (ROC): ROCs are possibly required when managing level 1 associations – sellers with more than 6 million yearly exchanges. It's gotten into the type of structure that is given by the PCI administrative body. At this level, any association is mindful of its anything but, a specific degree of an undeniable level of security. Security is dealt with truly at this level due to the degree of the harm of any information break or illicit utilization of client Visa information.

- Self-Assessment Questionnaire (SAQ): SAQs are those that assist associations with understanding their situating on PCI consistency. It's an obligatory method to review any association that receives the arrangements of PCI. The sort of SAQ that every association will be needed to finish relies upon the kind of seller they are and precisely how they handle Visa installments. For example, on the off chance that you re-appropriate installment interaction to a PCI – DSS consistent outsider, the idea of your poll would change.

We should investigate SAQ types.

SAQ A covers card-not-present traders (eCommerce and mail/phone orders - MOTO-installments) who have rethought all cardholder information capacities to PCI-consistent outsider installment specialist organizations, and don't measure, store or send any cardholder information on their framework premises. ASV checking isn't needed for SAQ A.

SAQ A-EP covers eCommerce shippers who have rethought all cardholder information capacities to PCI-consistent outsider installment specialist organizations, however, their site may affect the security of online installments. The dealer doesn't measure, store or send any cardholder information on their framework premises. SAQ A-EP requires ASV filtering.

SAQ B covers traders (barring eCommerce) utilizing just engraving machines with no advanced cardholder information stockpiling, and additionally essential dial-out terminals which interface straightforwardly to the telephone line instead of electronically. SAQ A-EP doesn't need ASV checking.

SAQ B-IP covers dealers utilizing just independent supported PIN Transaction Security (PTS) POS terminals with an IP association with the installment specialist organization with no electronic cardholder information stockpiling. SAQ B-IP requires ASV examining.

SAQ C covers traders (barring eCommerce) with installment applications associated with the web with no electronic cardholder information stockpiling. SAQ C requires ASV examining.

SAQ C-VT covers traders (barring eCommerce) with electronic virtual installment terminals given by a PCI-agreeable outsider installment specialist organization.

SAQ P2PE covers shippers (barring eCommerce) utilizing just equipment-based installment terminals remembered for and oversaw through an approved, PCI SSC-recorded Point-to-Point Encryption (P2PE) installment arrangement, with no electronic cardholder information stockpiling.

SAQ D covers shippers who have an immediate association with the installment specialist co-op and store card subtleties on their workers. It additionally covers all installment specialist co-ops characterized by a card brand as qualified to finish an SAQ.

PCI Compliance Checklist

These activities are important for the yearly PCI consistency agenda for dealers who don't utilize a facilitated installment arrangement. You likewise need to embrace security examines by an ASV each quarter.

- Complete the yearly Risk Assessment on the site page where the card information is dealt with or contacts the CDE.

- Guarantee outsiders that store, measure as well as communicate card information, or are associated with the CDE, give evidence that they are PCI DSS agreeable and are enrolled with the Card Schemes.

- If utilizing an outsider installment application in your site, you should guarantee the item and the form you are utilizing is PA DSS consistent (Payment Application Data Security Standard, which applies to designers of installment applications). Likewise, ensure you completely hold fast to the rules given by the provider.

- Train your staff to follow PCI-DSS methods.

- Ensure that you are just keeping fundamental installment information. Guarantee that all installment information is scrambled when communicated across open public organizations.

- Set up security controls to screen and control admittance to your eCommerce CDE.

- Defend touchy cardholder data by situating and keeping up firewalls and cutting-edge antivirus programming, preferably from a respectable producer.

- Guarantee that the shopping basket joining is the most exceptional rendition accessible.

- Secure your site security and examine with your web facilitating supplier to guarantee that they have gotten their foundation fittingly. Dealers ought to empower their web have up to please embrace framework solidifying principles and cripple default settings.

- Run yearly Pin Entry Device (PED) tests, and after any critical change to the CDE.

- Ensure that the seller of the product or equipment you use to handle exchanges has item endorsement from the Payment Card Industry Security Standards Council (PCI SSC).

Conclusion

PCI consistency is an essential piece of a business that acknowledges card installments. It can make a whole difference and make certain organizations look more appealing. Resolving to get exchanges for your clients consistently expands trust for your image and shields you from resistance charges and punishments. Getting to the nitty and coarse of PCI consistence can require time, exertion, and a huge spending plan, however, it positively helps your business' standing among shoppers and monetary organizations the same. Every business that handles card payments should pay attention to their PCI compliance – or risk suffering the consequences of a data breach.

FAQ

References

Subscribe for the latest news