Strong Customer Authentication (SCA)

In our digital age where everything is getting stored and performed online, one crucial priority becomes paramount -- securing online exchanges. This is where the idea of Robust Client Verification (RCV) comes to the forefront. This is a mandate set out in the Amended Directive on Payment Services or PSD2, which applies to transaction service suppliers across the European Economic Area. This newly established European regulation is in place to bolster the safety of online payments and minimize fraud susceptibility.

What is Strong Customer Authentication?

Understanding Robust Client Verification (RCV)

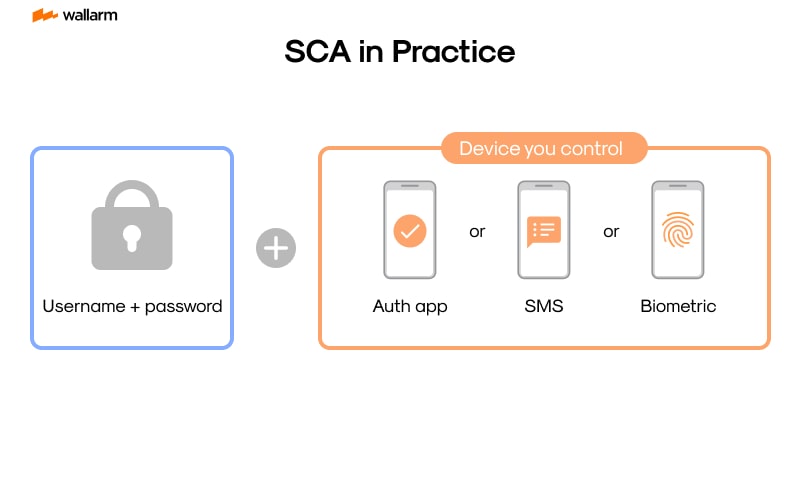

RCV is a mechanism that corroborates a user's essentiability for a service. It's a type of multi-element authentication that demands a minimum of two out of three components: a piece of knowledge known by the user such as a password, a physical item possessed by the user, for instance, a smartphone, or a personal attribute of the user like their unique fingerprint. This ensures that even if one element is breached, the bad actor would still have to overcome at least one more hurdle.

RCV's Significance

RCV creation is a response to the soaring instances of online fraud. An assessment by the European Central Bank revealed that, in 2016, card fraud led to losses amounting to approximately €1.8 billion. Through RCV, there is hope to dramatically sink these figures by introducing an additional shield to online exchanges.

How Does RCV Work?

In its practical form, RCV can occur in myriad ways. When performing an online purchase, a user might be asked to input a password (a piece known to them), and then verify the exchange via a smartphone application (a physical item they possess). Or, they could use biometrics like a fingerprint or facial recognition (a characteristic unique to them) to confirm their identity.

The Repercussions of RCV

The enforcement of RCV has serious ramifications for both business entities and consumers. For firms, it requires an overhaul of their transaction procedures to fall in line with the new guidelines. For consumers, this mandate will mean a slight alteration in the method of executing online payments, along with the inclusion of additional steps for identity verification.

RCV: The Road Ahead

As technology progresses, the means utilized for RCV will also witness evolution. Especially, biometrics are anticipated to hold a significant place in the future of RCV, with technologies like fingerprint and facial recognition making their way into regular use.

In conclusion, RCV proves to be an imperative stride in augmenting the safety of online transactions and diminishing fraud risks. While it may need few tweaks on behalf of businesses and consumers, the advantages of a fortified security system far overshadow the minor hindrances. As we tread into the digital era, RCV will assuredly keep transforming, offering even more potent protection for online transactions.

Why SCA is important in Today's Digital Era

Safeguarding Online Transactions: An In-depth Look at the Role of Multi-factor Authentication

The wave of digitization has swirled us into an era where e-payments are customary, and complex security tools such as Multi-factor Authentication (MFA) are not just luxuries, but necessities. Let's explore the profound influence of MFA in online transactions.

The Shift to Digital Payments

From the time internet paved its way into our lives, commerce has taken a revolutionary turn. Our daily errands like grocery shopping to sophisticated tasks such as financial management are increasingly carried out through digital payments. According to market forecasts, an astounding US$6,685,102m worth transactions are expected to occur through digital payments in 2021. This uptick in digital transactions has unfortunately invited a parallel upsurge in fraudulent dealings.

Combatting Digital Threats - Step-up Your Cybersecurity Game

With every stride towards a more digitized world, the likelihood of encountering fraud escalates. Savvy cyber-criminals constantly evolve their strategies to seize sensitive user data for illicit gains. A study by Javelin Strategy & Research in 2020 discloses that the losses to identity fraud breached $16.9 billion in 2019. These startling revelations emphasize the dire need for robust security solutions like MFA.

The Integral Part MFA Plays to Thwart Fraud

In the context of regulatory policies in Europe, MFA plays a pivotal role in fortifying e-payment security. It mandates businesses to corroborate the user's identity through more than one method of proof. This could encompass a unique password, possession of a specific device, or a distinct physical identifier like a fingerprint. This multi-tier verification mechanism dramatically curtails the likelihood of fraudulent incidents, making MFA invaluable in the fight against online deception.

Building Customer Confidence through MFA

Besides combating fraud, MFA can significantly augment trust and confidence among customers. A survey by Experian indicates that 55% of the users expressed an added level of trust if businesses adopted advanced security features like biometric identification. Implementing MFA is a testament to a business's commitment to safeguard customer data, which enhances their image and elicits customer support.

The Indispensability of MFA

MFA is no longer just an optimal security measure — it is a legal obligation. The Revised Payment Services Directive (PSD2) insists on the implementation of MFA for all e-transactions within the European Economic Area (EEA). Non-compliance can lead to severe financial penalties, making MFA imperative for business entities within the EEA.

Summing up, the escalating dependence on online transactions, growing cyber fraud threats, the urgency to foster customer trust, and the legal compulsion emphasizing MFA utilization together elevate the importance of MFA. As we continue to enjoy the comfort of online transactions, there emerges the continuous need for sturdy security shields like MFA.

The Pillars of SCA Explained

User authentication is of paramount concern for online security, acting as a safeguard for both individual and commercial interests against potential fraudulent acts. Of the many models, Strong Customer Authentication (SCA) distinguishes itself for its emphasis on three principal parameters - one's Cognizance, Assets, and Identity. Exploring these pillars helps to elucidate the efficacy and mechanism of SCA in defending online transactions.

Cognizance: The User's Exclusive Information

The first criterion of SCA, Cognizance, corresponds to exclusive information that the user keeps confidential. This could range from a password, a Personal Identification Number (PIN), or even a concealed query's response. The concept is to use information that remains private to the user, thereby making it challenging for a potential fraudster to obtain.

A common instance permits you to access your online banking platform by entering a unique username complemented by a password. Perceived as a knowledge-centric verification, the banking institution operates under the assumption that solely you possess this information. Consequently, a successful login signifies a high likelihood of an authorized access.

Assets: What the User Possesses

The second factor in SCA involves Assets, representing the tangible or intangible items a user possesses. These items could be physical, for instance, a debit card or a smartphone, or be virtual such as a software-generated token or a digital accreditation.

As a demonstration, consider online purchases. You could be requested to input a code transmitted to your phone. Because this kind of verification is predicated upon possession, the supposition is that only you, the genuine user, could have access to your device. A correctly entered code then points to your authorization.

Identity: Characteristics Unique to The User

The final factor under SCA is Identity, which resonate with unique attributes that define a user, such as a retinal scan, a voice tone, or a particular gestural pattern.

To illustrate, let's consider your smartphone unlocking pattern. If you're utilizing a retinal identification, then this is a case of identity-centric verification. If your distinctive retinal pattern is accurately recognized by the device, it likely denotes authorized access.

The Articulation of the Three Criteria

The potency of SCA dwells in the synchronization of these three criteria. By mandating at least two of them for successful user authentication, SCA exponentially secures user information or transactions against fraudulent activity. So, even if a miscreant should manage to crack your personal passcode (Cognizance), they would still require either your device (Assets) or the ability to duplicate your unique trait (Identity) to successfully bypass the SCA measures.

Here's a comparative exhibit detailing the three tenets:

In summary, understanding the triadic structure of SCA - Cognizance, Assets, and Identity - promotes a vigorous defense mechanism against cyber fraud. By decoding these elements, entities and users can significantly capitalize on the advantages of SCA and stay secure online.

Getting Started with SCA: A Comprehensive Guide

In the realm of online financial activities, protection stands utmost. A critical part of this protection matrix is referred to as Robust Client Confirmation (RCC). If you're trying to familiarize yourself with RCC, consider this detailed outline which explores its relevance, operations, and details on integrating it into your enterprise.

Grasping the Fundamentals of RCC

RCC, a stipulation stipulated in the Updated Norms on Payment Facilities (UPF) within the European Union, requires online transactions to be effectuated through multiple-proof identification to augment the protection around electronic financial movements. For the identification step, the user must use at least two proofs from the predetermined trinity of verification factors: cognition (a fact known to the user), ownership (an entity in the user's possession), and individuality (a distinctive feature of the user).

Method to Embed RCC

To integrate RCC into your enterprise, follow these steps:

- Evaluate your existing identification methods: Prior to introducing RCC, gain insight into the identification methods already being utilized. This analysis will highlight gaps and pinpoint alterations in need.

- Select an RCC system: Numerous RCC systems are accessible. Your selection should accommodate your enterprise's requirements and be consistent with governing regulations.

- Merge the RCC system: After picking an RCC system, merge it with your current operations. This step might necessitate specialized assistance, so consider involving your IT department or employing a specialist.

- Examine the RCC system: Post-merging, conduct an examination of the RCC system to ascertain its performance. This preemptive step will help detect any problems before customers are affected.

- Educate your team: Members of your team should be able to grasp the functioning of the RCC system, including efficient handling of potential issues. This understanding will ensure smooth transitioning and mitigate the chances of business disturbances.

- Incorporate the RCC system into customer activities: Once you've set up everything, the RCC system should be introduced to the customers. Transparent communication with customers about these modifications and their effects is prudent.

Picking the Ideal RCC System

When deciding on an RCC system, remember these considerations:

- Regulatory Consistence: The system must conform to regulatory mandates. This requirement is absolute.

- User Friendliness: The system must be straightforward and convenient for your customers, or else it could result in client dissatisfaction and subsequent discontinuation.

- Harmonious Incorporation: The system should merge effortlessly with your current operations, thus mitigating any business disruptions.

- Pricing: The affordability of the system, both immediate and long-term, should be deliberated upon.

- Assistance: Your solution provider should offer effective support to aid with potential problems.

In essence, the introduction of RCC represents an indispensable move in fortifying your online financial transactions. With a keen understanding of RCC's basics and following the method delineated here, you can achieve successful incorporation.

Understanding the Regulatory Landscape around SCA

The intricate and ever-changing domain of Strong Client Verification (SCV) is dictated by various factors including the rise in digital exchanges, the progressive complexities of cyber threats, and the necessary sturdy protection of consumers. This section aims to extensively cover the regulatory framework overseeing SCV, underlining the crucial laws, effects and the steps businesses can take to effectively steer through this intricate terrain.

Worldwide Legislation: A Comprehensive Synopsis

Internationally, several authoritative entities have put forth rules and norms regarding SCV. The most noteworthy being the Digital Transaction Regulation 2 (DTR2) deployed by the European Union. DTR2 necessitates the use of SCV for every electronically processed transaction within the EU’s jurisdiction. Additionally, DTR2 also introduces specific stipulations for the introduction and operation of SCV, underlining the essentiality of at least two independent verification factors.

In The United States, the National Financial Resilience Body (NFRB) has publicized advice on the utilization of multi-verification factors, similar to SCV. The recommendation suggests financial bodies should employ multi-verification methods for high-stake transactions.

In Asia, Singapore's Financial Pioneer Authority (FPA) has circulated advice on the application of SCV to online finance transactions. The advice suggests the employment of a minimum of two verification factors and offers specific advice on the diverse range of verification categories that can be employed.

Deep-diving into DTR2 and SCV

The DTR2 legislation has revolutionized the sector of digital security. It not only mandates the application of SCV but also lays out specific protocols for its operation. In compliance with DTR2, SCV requires at least two independent verification factors from the following categories: cognition (something the client is aware of), ownership (something the client possesses), and uniqueness (something the client embodies).

The legislation also introduces specific advice on the operation of dynamic links, a method that associates the verification process with an unchangeable amount and payee. This security measure ensures that even if the verification data is illicitly procured, it cannot be manipulated to process unlawful transactions.

Steering through the Regulatory Terrain: Crucial Notes for Businesses

While it can be demanding for businesses to maneuver through the intricate regulatory framework of SCV, the adoption of a few key measures can facilitate this process:

- Comprehend the Legislations: The initial step involves gaining comprehensive knowledge of not only universally binding laws such as DTR2 but also any local legislation that governs your line of business.

- Execute SCV: Upon understanding the legislation, the subsequent step entails the incorporation of SCV in adherence to these legislations. This involves selection of appropriate verification factors, introduction of dynamic links, and ensuring a user-friendly verification process.

- Stay Informed: The legislative guidelines governing SCV are constantly altered and improved. Hence, it's crucial to be apprised of the current amendments and adapt your SCV strategy accordingly.

To conclude, although the regulatory framework surrounding SCV may seem labyrinthine, it's surmountable. By comprehending the laws, effectively incorporating SCV, and staying abreast of emerging developments, businesses can guarantee compliance and safeguard their clientele from potential online deceit.

How SCA is Reshaping Online Security Architecture

An uptick in digital protection measures has become evident with the adoption of Enhanced Client Verification (ECV). This shift is predominantly steered by the urgency to bolster online transaction security and undercut the incidence of illicit activities. ECV's emergence spearheads the application of a complex security technique requiring verification through a minimum of two separate factors categorized as Personal Intel, Ownership, and Identity Trait.

Evolution from Singular to Composite Verification

In the past, online protection hinged largely on singular verification mechanisms, predominantly conventional password-based systems. However, the evolving intricacy of digital threats dictated a firmer protective measure. ECV, offering composite verification, supplies this much-required security enhancement.

In the paradigm of singular verification, the integrity of an online operation solely depends on the strength of a password. If a nefarious entity somehow cracks the password, they singlehandedly acquire unlawful access. However, ECV requisites authentication through a minimum of two unrelated factors. Even if one factor gets breached, the offender still needs to circumvent the other factor(s), thereby making illegal access phenomenally difficult.

ECV's Foundational Triad

ECV bases itself on a triad: Personal Intel (data only the user is aware of), Ownership (an item only the user possesses), and Identity Trait (unique distinctive characteristics of the user). Each triad member serves as a distinct verification element, and any ECV operation must employ at least two of them.

- Personal Intel: This encompasses information exclusive to the user, like a password, unique number, or secret query response.

- Ownership: This makes use of an item only the user possesses, for instance, a mobile gadget, smart chip, or security key.

- Identity Trait: This consists of a distinctive inherent quality peculiar to the user—for example, a thumbprint, vocal trait, or facial pattern.

Requiring a minimum of two of these factors, ECV assures a more potent security level than conventional singular verification methods.

Alterations in Digital Security Structure

ECV implementation demanded modifications in digital security structure, including:

- Strengthened User-Proofing: With ECV, user-proofing processes have become stringent, leading to the invention of cutting-edge user-proofing tech, such as identity trait verification and device ID capture.

- Boosted Data Protection: ECV mandates the secure transmission and archiving of verification data, pushing for the utilization of next-gen encryption tech and secure data transfer methods.

- Amplified Mobile Device Usage: With ECV, mobile devices as a verification element have seen increased usage, consequently resulting in the creation of mobile-based verification applications and the integration of mobile devices into the digital security structure.

Technology's Contribution to ECV

ECV executions have been made feasible due to technological progress. Identification trait tech, like thumbprint scanners and facial recognition systems, have enabled the utilization of Identity Traits for authentication. Likewise, the prevalent use of mobile gadgets and the creation of mobile-based verification apps allowed the use of Ownership as a verification element.

In sum, ECV is remodeling digital protection structures via the introduction of a multi-tier security method. This method, needing verification through a minimum of two unrelated elements, offers a better security level than traditional singular verification ways. With the continuous surge in tech advancements, we can anticipate witnessing even more advanced ECV techniques in forthcoming times.

SCA Compliance: What Businesses Need to Know

To thrive in the digital arena, Strong Customer Authentication (SCA) conformity is a vital requirement. Staying current with the dynamic rules and norms in the field is essential for businesses to remain lawful. We will delve into key areas that need consideration: the primary criteria for SCA compliance, how companies can achieve precise accordance, and the possible implications of non-conformance.

Tenets of SCA Compliance

SCA compliance anchors on three main constituents, sometimes referred to as the SCA trinity.

- Knowledge: Represents data that the customer alone should know, such as security codes or secret answers.

- Possession: Stands for an object or a digital element that the customer uniquely owns, examples can be a credit card or a unique-token generating app.

- Inherence: Highlights specific characteristics unique to the customer, like an iris pattern or voice modulation.

In order to fall in line with SCA norms, a company needs to set up a dual-factor verification method integrating a minimum of two from the above-mentioned constituents.

Pathway to SCA Compliance

The passage towards SCA lawfulness requires several key stages:

- Evaluation: The onset involves a rigorous enquiry into the prevailing security techniques and identification of gaps to be bridged. This encompasses an in-depth analysis of the authentication mechanisms to confirm their synchronization with SCA norms.

- Implementation: The succeeding phase deals with the execution of the identified reforms which could span from system enhancements, application of avant-garde technology, or an alteration in operational procedures.

- Inspection: After the modification phase, it’s crucial to inspect the systems to ensure smooth operation and efficacy. This calls for intense testing and troubleshooting if necessary.

- Monitoring: Post-implementation, constant vigilance is critical to assure sustained adherence to guidelines. This requires companies to periodically audit their procedures and systems, and make the needed adjustments.

Implications of SCA Non-Adherence

Infringing SCA compliance can incite severe repercussions, which may extend from monetary sanctions, legal action, up to jeopardizing your payment settlement facilities. The specific implications invariably rely on the jurisdictional rules of your operational area and the severity of non-adherence.

To conclude, being SCA-compliant is a pivotal obligation for firms functioning in the digital ecosystem. By understanding the core principles and deploying suitable actions, companies can fulfil their legal obligations while safeguarding their customers' confidential details.

SCA and Its Relation to PSD2

Residing within the domain of web-based fiscal operations, two significant regulatory directives have established prominence - the robust mechanisms offered by SCA (Strong Customer Authentication) and the regulatory framework elucidated by PSD2 (Payment Services Directive 2). Together, they bring revolutionary transformations in enhancing transactional safety mechanisms. To decode this intricate relationship between SCA and PSD2, we need to distill each concept to its essence.

Glancing at PSD2

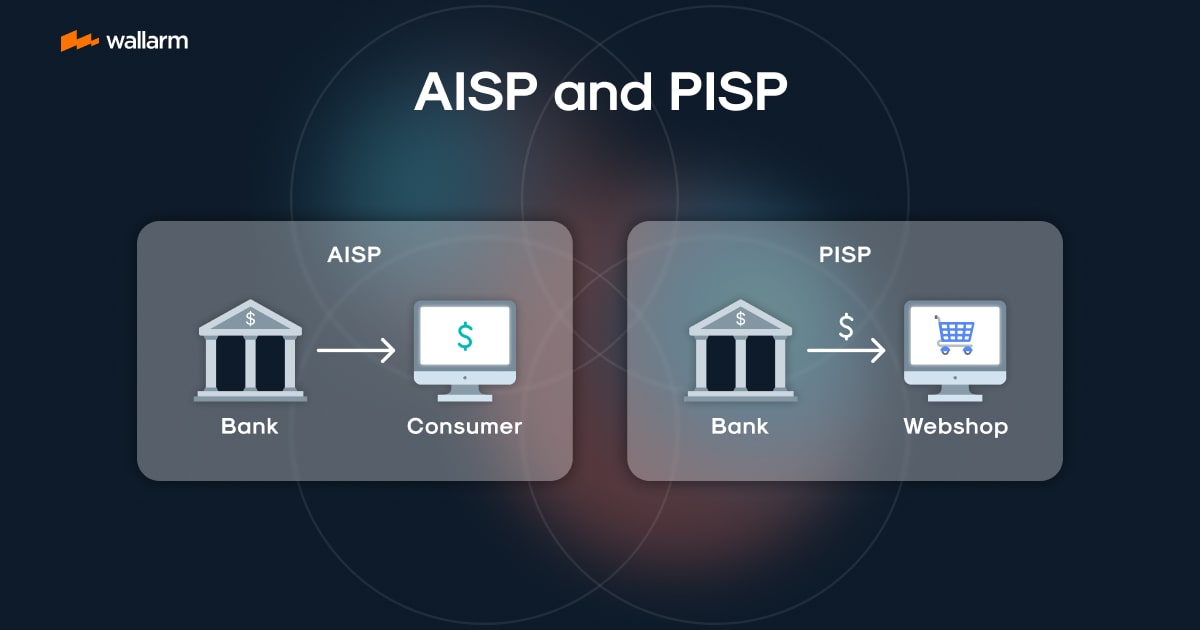

PSD2, a legislative framework curated by the Europeans for regulating operations in digital payment domains, aspires to fill the security gaps in monetary transactions across Europe. Simultaneously, it acts as a catalyst to spur innovation and prompt the fiscal sector to remain in step with the newer technological advancements. The highlight of PSD2 is its mandate requiring banks to provide access to their transactional infrastructure and client-centered database to third-party players. This directive has fueled a notable surge in 'open banking' amenities that champions customers to have a stronger hold over their financial data.

SCA's role within PSD2

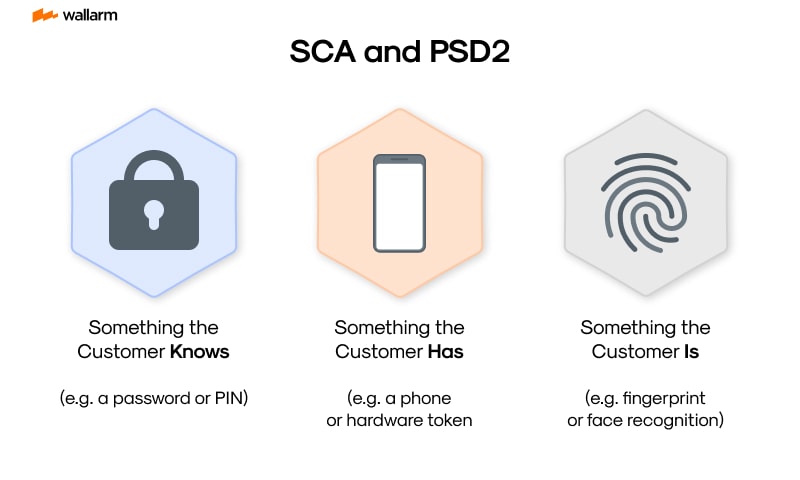

SCA surfaces as an inextricable element of the PSD2 framework. As per this mandate, SCA becomes mandatory for all web-based transactions enacted within the European Economic Arena (EEA). This mechanism aims to quash fraudulent activities and fortify the security of online payment systems. To meet this aim, SCA proffers an authentication model that relies on two out of these three components:

- A knowledge-based component (for instance, passwords or PINs)

- A possession-based component (for instance, a mobile device or security token)

- An inherent component (for instance, biometrics like fingerprint or facial configuration)

Often referred to as two-factor authentication (2FA), this model significantly trims down scams and fraudulent activities.

The Nexus between SCA and PSD2

The relationship shared by SCA and PSD2 is reciprocal. While SCA contributes a stringent security framework to fortify open banking services, in turn, the PSD2 relies on SCA as the backbone of its mandate.

The Business Implications

For enterprises, the SCA-PSD2 marriage brings along both difficulties and new opportunities. On the downside, they must integrate reliable SCA solutions adhering to PSD2's mandate, a process likely to be intricate and costly. However, on the bright side, the open-door policy promoted by PSD2 could pave the way for more creative and customer-centric financial services.

Charting the SCA-PSD2 Terrain

For any business navigating the digital transactional domain, understanding the salient features of the SCA and PSD2 relationship is vital. Regulatory compliance should not merely be viewed to evade penalties—instead, it opens fresh avenues for more reliable, innovative services.

In summary, SCA and PSD2 are two pillars supporting the same structure. Jointly, they are restructuring the online payment ecosphere — making it not only more secure but also customer-friendly. As these regulations continue to morph, businesses must remain informed and flexible to successfully navigate the ever-dynamic landscape.

In-Depth Analysis of SCA Protocols and Standards

Digital safety and transactional integrity has become intertwined with multifaceted rules and guidelines aimed at bolstering the security of online operations. A game-changing evolution in this arena can be seen in the emergence of Tough User Recognition (TUR) principles. Let's journey into the depths of TUR codes of conduct, unraveling their function and repercussions.

Inspecting the TUR Protocols

TUR protocols essentially serve as the spinal cord of the identification process, sketching out the critical steps needed to confirm a user's identity. The central protocol adopted within TUR is the Enhanced Three-Dimensional Security Version 2.0 (E-3DS2), superseding its predecessor, the Three-Dimensional Secure (3DS).

E-3DS2 is conceived to bolster the security of virtual transactions while streamlining the user journey, diminishing the dependence on extraneous verification hurdles. It accomplishes this by facilitating a broader exchange of information between vendors and card-issuing entities, resulting in superior risk evaluation and more strategic decision-making.

The protocol comprises three distinct stages:

- Info Gathering: This entails the vendor compiling details about the transaction, like the apparatus used, the location, and transactional history.

- Risk Calculations: Based on the supplied information, the card-issuing entity gauges the riskiness of the transaction.

- Identity Confirmation: Should the transaction pose a substantial risk, the issuer would seek additional proof of identity from the user, like a password, fingerprint, or a single-use code.

TUR Standards: Uniformity and Adherence

Regulatory authorities design TUR standards to drive uniformity of identification tactics across the sector. The most prominent being the Updated Payment Services Directive (PSD2), courtesy of the European Financial Oversight Authority (EFOA).

PSD2 commands all electronic transactions within Europe's economic zone to utilize TUR. It stipulates that any two of the three following elements must be used for user confirmation:

- Cognition: Something familiar to the user, like a password or pin code.

- Ownership: Something possessed by the user, for instance, a phone or a physical token.

- Uniqueness: An inherent feature of the user, such as a fingerprint or facial features.

It's this requirement that has given rise to the "dual-factor ID confirmation" or "2FA" theme behind TUR.

Contrasting TUR Protocols and Standards

The Interworking of Protocols and Standards

TUR protocols and standards operate in synchrony, creating a secure and reliable framework for identification. The protocols furnish the technological tools for executing the standards, while the standards ensure the harmonious and effective application of these protocols.

In conclusion, TUR protocols and standards are vital for bolstering digital security. A comprehensive understanding of their operation empowers businesses to deftly traverse the digital terrain and deliver a secure and fluid experience to their clientele. With the steady evolution of technology, these protocols and standards will continually adapt, laying the foundation for increasingly secure online operations in the years to come.

Technical Breakdown: How Does SCA Work?

The principle of Robust User Confirmation (RUC) is embedded within European regulations, devised specifically to fortify the trustworthiness of online monetary dealings. This concept propels businesses to confirm their customer's identity by executing dual autonomous validation processes, more commonly referred to as dual-stage authentication (DSA). This validation ought to come from two distinct sectors: a factor that the customer is privy to (say, a secret code), a factor which the customer physically possesses (like, a mobile device), or a factor that is inherently related to the unique identity of the customer (like, biometric data).

Steps within RUC

Any transaction initialized by a customer triggers the Payment Service Provider (PSP) to analyze the transaction to gauge if enacting RUC is compulsory, governed by the risk factor associated with the transaction. In the event RUC execution becomes obligatory, the PSP requests the necessary dual validation passcodes from the customer.

Here is a brief walkthrough of the RUC execution:

- A customer initiates a transaction.

- The PSP assesses the transaction for potential risks, and subsequently, the need for RUC.

- If RUC is deemed essential, the PSP requests the customer to provide dual validation passcodes.

- The customer provides the necessary validation passcodes.

- The PSP then verifies these passcodes.

- Should the passcodes be authenticated, the transaction progresses. If authentication fails, the transaction is discarded.

Inclusion of 3D Secure 2 in RUC

3D Secure 2 (3DS2), a specified protocol, is a key component in RUC execution. It forms a liaison between businesses and card issuers to attest transactions with authentication. 3DS2 ensures transactions with minor risk can be authenticated without needing active customer participation.

Below is a brief of 3DS2's role within RUC:

- The customer initiates a transaction.

- The merchant communicates transaction details to the card issuer via 3DS2.

- The card issuer assesses the transaction's riskiness.

- If deemed as low-risk, the issuer independently validates the transaction, or otherwise requests the customer for dual validation passcodes.

- The customer then provides these passcodes.

- The issuer verifies these passcodes.

- Upon successful verification, the transaction is allowed to proceed. If verification fails, the transaction is discarded.

Impact of RUC in Open Banking Network

The Open Banking structure enables banks to share customer information with third-party providers or TPPs by leveraging Application Programming Interfaces (APIs). RUC ensures that TPPs can access customer information only after the customer's identity has been verified by providing dual validation passcodes.

The elucidation of RUC's role in Open Banking is as follows:

- The customer initiates a transaction with a TPP.

- The TPP seeks access to customer's banking information.

- The bank then requests the needful dual validation passcodes from the customer.

- The customer provides these passcodes.

- The bank verifies these passcodes.

- Once the verification process is successful, the bank reveals the requested data to TPP. If the process fails, the data request is discarded.

Conclusively, by insisting on verifying customer identities through unbiased validation processes, RUC amplifies the security integrity of online transactions and remarkably enhances safeguarding measures against fraudulent activities. Whether this is realized via 3DS2 or the Open Banking model, RUC is redefining the methodology for user authentication in digital security.

The Role of Biometrics in SCA

Bio-Security gadgets bring a new age of ideology in the realm of discerning personal identity techniques. Relying on aspects peculiar to human beings, these ground-breaking approaches provide a sturdy and infallible medium of verification, embracing sincerity with reliability.

Upgradation of Bio-Security Methods Improving Identity Validation System

The persistent evolution of bio-security applications paves the way for superior assessments of individual's body particulars and distinctive behaviors. Verification methods employ distinct identifiers like fingerprint impressions, unique facial attributes, verbal intricacies, retinal designs and rhythm of typing. When compared to traditional identity pointers like alpha-numeric passwords and pin codes, bio-security identifiers prove to be unique and complex to duplicate, providing a more secure and fail-safe validation process.

Bio-security markers are proven game-changers in identifying user identities, trumping over orthodox verification entities like pin-centric systems or device-centric properties such as gadget emblems.

Bio-Security vs Conventional Verification Techniques

A detailed examination of various bio-security methods as compared to conventional authentication techniques pinpoints the remarkable endurance of bio-security systems.

Even with some limitations, the incorporation of bio-security elements into personal identification procedures unfolds exclusive benefits, embodying a dexterous equilibrium between facilitating security and user convenience.

Implementing Bio-Security Processes for User Authentication

Different bio-security processes used for confirming identities have their respective strengths and shortcomings:

- Fingerprint Checks: The singularity and worldwide applicability of fingerprints make them a highly favored mode of personal authentication. However, external factors like filth or skin diseases can compromise their effectiveness.

- Face ID Authentication: This process validates users by recognizing distinct facial alterations. While most devices can seamlessly integrate with this method, variable lighting conditions or physical changes can affect its performance.

- Verbal Command Authentication: This method is dependent on particular voice features. Its flexibility notwithstanding, environmental noises or changes in voice can impact its precision.

- Retinal Blueprint Confirmation: This approach certifies identities based on retinal patterns. Though it boasts of exceptional accuracy, it requires special instruments and might not work efficiently with eyewear.

Successful Adoption of Bio-Security into Identity Verification

The transition of integrating bio-security into an existing validation structure necessitates several key steps:

- Selecting the Suitable Bio-Security Method: Perform thorough investigations considering the required security protocols, user preferences, and device constraints.

- Compiling Bio-Security Data: This pivotal stage includes the collection and secure storage of the user's bio-security data.

- Bio-Security Data Protection: It is essential to ensure that stored bio-security data is safeguarded from unauthorized access.

- Regular Authentication: This measure involves consistent retrieval and analysis of users' bio-security data during validation to confirm their identity.

In summary, bio-security methods provide significant benefits for user authentication courtesy of their uniqueness and superior security quotient. However, it's essential to properly manage data security and privacy issues. With the growing interest in bio-security technology, a significant shuffle in user authentication methodologies is anticipated.

The Future of SCA and Online Security

Peering into the digital horizon, it's evident that Advanced User Validation (AUV) will become a cornerstone of future online safety measures. Amid the swift pace of tech enhancements and escalating complexity of digital risks, a dynamic, fortified approach to security is crucial, asserting AUV's indispensable role in this transforming landscape.

AUV's Progressive Journey

AUV isn't a rigid notion but evolves constantly keeping pace with the surging digital challenges and progressions. Biometric identification like fingerprint and facial mapping, and cutting-edge technologies as AI and machine learning will increasingly shape AUV's trajectory.

On account of their distinctiveness and difficulty to duplicate, biometric technologies like fingerprint and facial scanning are increasingly being recognized as standard AUV tools. The scope of biometrics in AUV will expand to accommodate more advanced identifiers, such as iris and vascular pattern recognition technologies.

The role of AI and machine learning in upcoming AUV systems will also grow substantially. These advancements allow behavior pattern tracking and unusual activity detection, potentially spotting deceitful activities. This preemptive method can avert security compromises, establishing these technologies as essential components of the AUV set-up.

AUV and Blockchain: A Promising Alliance

A notable stride in the AUV sector is the integration with blockchain technology. Blockchain’s distributed, irreversible feature makes it a fitting base for dependable verification. Future AUV models could incorporate blockchain, offering a safe, transparent, and inviolable verification process for user identities.

Preparing for the Quantum Race

Quantum computing, although in its nascent stages, holds enormous promise for the AUV realm. Quantum machines, owing to their extraordinary speed, can process data volumes far surpassing conventional computers, thereby expediting the analysis of extensive security data. However, the arrival of quantum computing poses fresh hurdles for AUV, as these formidable processors might decipher conventional security encryptions. Consequently, the AUV growth trajectory may require the formulating of quantum-resistant encryption codes.

Unfolding the Future of AUV: A Safer Cyberspace

In summing up, the future scenario for AUV seems full of potential. Technological breakthroughs such as AI, machine learning, blockchain, quantum computing, and biometrics are set to fortify AUV further. These enhancements, however, pose new hurdles requiring proactive solutions to maintain the effectiveness of AUV.

As we march on toward this new era, it is vital for corporations and individuals equally to keep abreast of the latest progress in AUV and internet safety. By doing so, each of us can contribute to engineering a more robust, secure digital ecosystem.

Understanding the User Experience in SCA

The interaction a user has with any online security measure, such as Strong Customer Authentication (SCA), can significantly sway their perception towards it. It's safe to say that UX, short for User Experience, in SCA, is an indispensable facet that determines its effectiveness.

The Role UX Plays in SCA

UX in SCA entails more than merely facilitating a smooth authentication journey. The optimum UX finds delicate equilibrium between engaging user interaction and robust safeguards. If tailored correctly, SCA can earn the user's trust, bring down drop-offs, and enhance the probability of conversions. Alternatively, a less-than-satisfactory design can provoke user dissatisfaction, causing transaction desertions and consequent revenue loss.

SCA's Effect on UX

Embedding SCA means incorporating an extra level of digital safety while transacting online. This addition may complicate the user's journey by necessitating at least two distinct validation elements stemming from what they possess (like a smartphone), or what they can recall (like a passcode), or even their physical traits (like fingerprints). The complexity can stretch the transaction time, a scenario some may find unpalatable.

Nevertheless, businesses can devise SCA tactics that instead of detracting from the UX, enrich it - provided they apply strategic foresight and meticulous implementation.

Giving UX a Boost in SCA

Businesses can leverage a plethora of methods to elevate UX in SCA. A few critical ones include:

- Brevity in Authentication Procedure: The SCA journey should be condensed and instinctive. Evade intricate systems and esoteric lingo that may perplex users.

- Transparency in Instructions: Forewarn users with all requisite steps for successful authentication. Concise directives should serve this purpose.

- Favor Familiar Modes of Authentication: Opt for verification procedures that users easily relate to. This can minimize their necessity to learn something new and lead to a more manageable process.

- Offer a Wide Array of Authentication Options: Cater to the individuality of users by providing an assortment of authentication options, which can enhance their experience.

- Elevate Efficiency in Authentication: Ensure that the authentication procedure is prompt and proficient. Delays can annoy users and provoke transaction desertions.

- Mobile Experience Claims Priority: With the escalating use of mobile devices for online transactions, it's paramount that the SCA mechanism is compatible with the mobile interface.

How Biometrics Contributes to UX

Implementing biometric authentication, which falls under the 'what they are' SCA category, can substantially uplift the UX. Biometrics like fingerprint or face identification offer security and convenience simultaneously, negating the need to remember passcodes or carry extra devices.

The Path of UX in SCA

As advancements in Artificial Intelligence (AI) and Machine Learning technologies continue to unfold, the UX involved in SCA will also modernize. Emerging technologies like Behavioral Biometrics, which studies repeated patterns in user behavior for authentication, bear immense potential.

As a wrap-up, the integration of SCA may render an additional layer of security to online transactions, but with thought-out strategies and solid execution, it can act to augment both the security and overall UX, proving to be advantageous for businesses.

Case Study: Successful Implementation of SCA

In the digital security landscape, the adoption of Enhanced User Verification (EUV) is transforming how transactions are handled. This case study examines the successful utilization of EUV by a prominent online retailer, referred to as "Enterprise Y" to protect identities.

Recognizing the Problem

Enterprise Y, an international online retailer, grappled with the increasing issue of deceptive transactions. The company's present defenses proved inadequate against advanced digital threats. The inability to curb such fraudulent activities resulted in a substantial financial drain and eroding customer faith.

Committing to EUV

Faced with escalating frauds and to meet the specifications of the Revised Payment Service Directive (RPD2), Enterprise Y opted for EUV as an effective solution. The choice was dictated by the need to diminish bogus transactions and regain customer confidence.

Details of the Adoption

The process of adopting EUV was structured and systematic.

- Supplier Selection: Enterprise Y initially selected a supplier with EUV expertise. The decision was influenced by the supplier's experience, proven performance, and the ability to tailor the solution to Enterprise Y's distinct requirements.

- Tailoring: The EUV solution was adjusted to the company's transaction workflow, including a two-step verification process for transactions above a specified amount.

- Integration: Following customization, the solution was incorporated into the existing transaction system, ensuring a smooth transition through rigorous testing.

- Instruction: Enterprise Y undertook comprehensive training for its workforce to enable them to proficiently operate the new system and competently address EUV-related customer inquiries.

- Customer Outreach: Enterprise Y updated its customers on the new arrangements via numerous channels such as emails, social media, and on its website, acquainting them with EUV and its implications on trades.

The Impact

The utilization of EUV radically modified Enterprise Y's operations.

- Bogus Transactions Minimized: Two-step verification made unauthorized transactions more challenging to execute, resulting in a steep decline in deceptive transactions.

- Compliant to Regulations: Successfully adopting EUV allowed the enterprise to satisfy RPD2 specifications, saving potential penalties while emphasizing its dedication to secure customer transactions.

- Customer Confidence Restored: The use of EUV effectively rebuilt customer trust as customers welcomed the added layer of security and felt safer when conducting transactions.

Lessons Gleaned

Enterprise Y's successful adoption of EUV imparts valuable insights for other businesses.

- Supplier Selection's Crucial Role: It is imperative to choose a supplier with an extensive understanding of EUV who can adjust the solution to the company's unique requirements.

- The Requirement of Education: Ensuring a smooth shift to a new system necessitates thorough employee training.

- Significance of Customer Briefing: It is vital to keep customers informed about the changes and how it impacts their transaction process.

To sum up, adopting EUV can substantially bolster a business's security protocols, slash deceptive transactions, and revive customer faith. To ensure a successful transformation, it is essential to have thorough planning, skilled vendors, comprehensive employee education, and effective communication with customers.

Decoding SCA: Final Takeaways and Future Prospects

Wrapping up our detailed probe into Strong Customer Authentication (SCA), let's mull over the chief insights and envision the prospective trajectory of this indispensable safeguard.

The Necessity for SCA

Unveiling itself as a pivotal element in the arena of internet safety, SCA isn't merely a norm laid down by the Revised Payment Services Directive (PSD2) in the European Union. It transcends those statutory borders, focusing primarily on shielding patrons and businesses from deceitful actions, bolstering confidence in web-based transactions, and nurturing a more secure virtual environment.

Cardinal Insights

- Legislative Adherence: SCA isn't merely an advisable practice; it is a ruling directive for businesses functioning under the EU. Infringement can incur punitive measures and harm the entity's public image.

- Falconlike Security: By needing multiple identification stages, SCA considerably lessens the chance of deceit, making it challenging for those with foul intentions to obtain delicate data.

- User Friendliness: Even though SCA enhances security, it's essential to facilitate it in such a manner that doesn't disrupt the end user's convenience. Striking the right equilibrium between security and user-friendliness is pivotal to the successful implementation of SCA.

- Technological Revelation: The advent of SCA has fanned the flames of innovation in verification mechanisms, embracing biometrics and machine learning algorithms. These breakthroughs are rendering SCA more secure and easier to handle.

Prospective Developments

Gazing into the future, it's clear that SCA will continue to evolve, adapting to emergent risks and tech developments. Here are some tendencies to keep an eye on:

- Biometrics: As biometric mechanisms become more intricate and universally accepted, they will occupy a more significant spot in SCA. Biometrics deliver a high-security level without sacrificing user convenience.

- Artificial Intelligence (AI): AI and machine learning can take SCA to new heights by evaluating user activities and flagging unusual patterns that might hint at fraudulent activity. This makes SCA more potent and less invasive.

- Regulatory Evolution: As cyber threats change and advance, the legislative landscape will follow in step. Companies need to keep up with SCA requirement amendments to maintain adherence and safeguard their patrons.

- Worldwide Acceptance: Although SCA is currently mandatory in the EU, it's plausible that other regions might adopt similar rules in the future, reinforcing SCA's worldwide significance.

In summary, SCA is an essential shield in the battle against cyber fraud. Its relevance will only amplify as digital transactions multiply and web threats escalate. Businesses need to view SCA not merely as a legislative prerequisite but as a cardinal strategy that amplifies trust, safeguards clients, and fuels growth.

FAQ

References

Subscribe for the latest news