Open Banking API: How It Works, Use Cases & Selection Guide

The digital age brings a significant shift in conventional banking systems, giving way to Open Banking API methodologies. These advanced procedures augment the financial sector by providing diverse functionalities, catering superbly to the growing requirements of both private and business concerns.

Evolution from Classic to Advanced Open Banking Protocols

Earlier, banks suffered from limited reach and dull customer interactions. However, this landscape has transformed with the adoption of new-age open banking techniques. This momentous change owes to the incorporation of emerging technologies which cater to the evolving client preferences, and revamped regulatory guidelines.

Open Banking emphasizes transparency, mutual respect, and accessibility. It lays out a platform for freelance coders to access a wealth of banking data via APIs (Application Programming Interfaces), leading to the creation of distinct financial products and solutions.

Primary Elements of Open Banking API – A Closer Examination

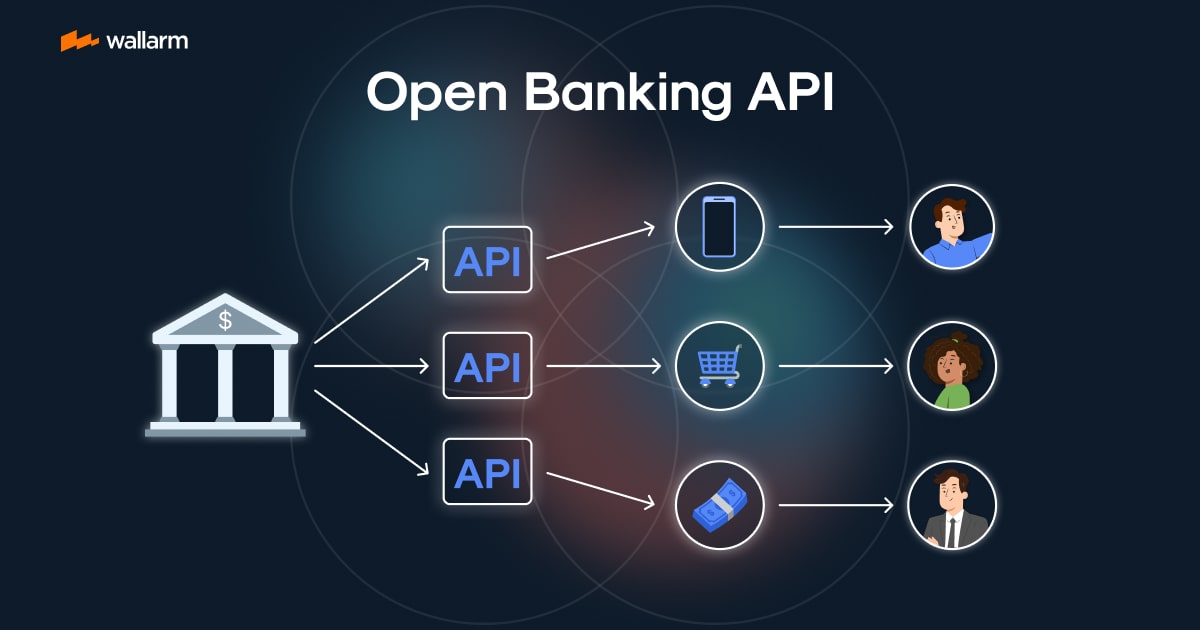

The Open Banking API, a crucial component of this banking upheaval, serves as a catalyst for change. It erects a communication channel between financial institutions and independent app developers, thus facilitating an efficient data exchange.

The API carves a secure pathway for banks to share their proprietary data with verified third-party service providers. The shared data might comprise specific details such as banking credentials, comprehensive transaction logs, and payment histories. Simultaneously, the API equips external coders with the necessary apparatus to craft agile banking applications and services, thereby broadening the customer interaction channels for banks.

The Benefits of Open Banking API Integration

Integrating Open Banking API offers an array of benefits for all parties involved. For financial institutions, it stirs innovation, boosting their relevance in a swiftly digitalized milieu and sharpening their competitive edge by capitalizing on third-party expertise.

For software developers, Open Banking provides easy access to a multitude of financial data that can be utilized to develop revolutionary applications. Moreover, it establishes a feasible route for closer collaboration with financial entities, thereby ramping up operational efficiency.

Customers are ultimately the biggest winners in this Open Banking revolution. The APIs incorporate multiple financial solutions onto a single platform, offering users the ease of comprehensive financial management.

The Impact of Open Banking API Application

Consider an instance where a developer exercises the Open Banking API to design a bespoke financial management application. The app could merge data from several financial institutions, offering the user a consolidated view of their finances. It could incorporate functions such as budget management, expense tracking mechanisms, and tailored financial advice, guiding users towards informed financial choices.

Implementing Open Banking API triggers digital metamorphosis in the banking industry. It nurtures a cooperative and transparent ethos while enhancing customer gratification. This unfolds a powerful financial services landscape, revealing unexplored opportunities for all participants.

Grasping the Key Elements of Innovative Banking API

In a nutshell, Banking API is an instrumental portal that arms external developers with the ability to construct utilities and amenities anchored in specific financial institutes. Here are the crucial components:

- Channelling Information: The primary role of Innovative Banking API is about the safe and secure relay of customer data. It permits banking institutions to relay consumer information to approved TPPs. The shared details touch on account data, transactional records, and specifics of payments.

- Protection Mechanisms: Innovative Banking API is designed with stringent security measures to safeguard financial data. Encryption, tokenization, and dual-factor authentication are integral to these protocols.

- Uniformity: To ensure smooth interaction between distinct financial bodies and TPPs, Innovative Banking API observes particular standards. In the UK jurisdiction, the foundation of these standards is the Open Banking Implementation Entity (OBIE).

- Legal Guidelines: The Innovative Banking API operates under a set of rules that prioritize consumer protection and data privacy rights. It's the Financial Conduct Authority (FCA) in the UK that provides this regulatory setup.

Diving into the Intricacies of Innovative Banking API

Innovative Banking API isn't a single unit but rather a combo of several API models, each with a distinct role. Here are three primary types:

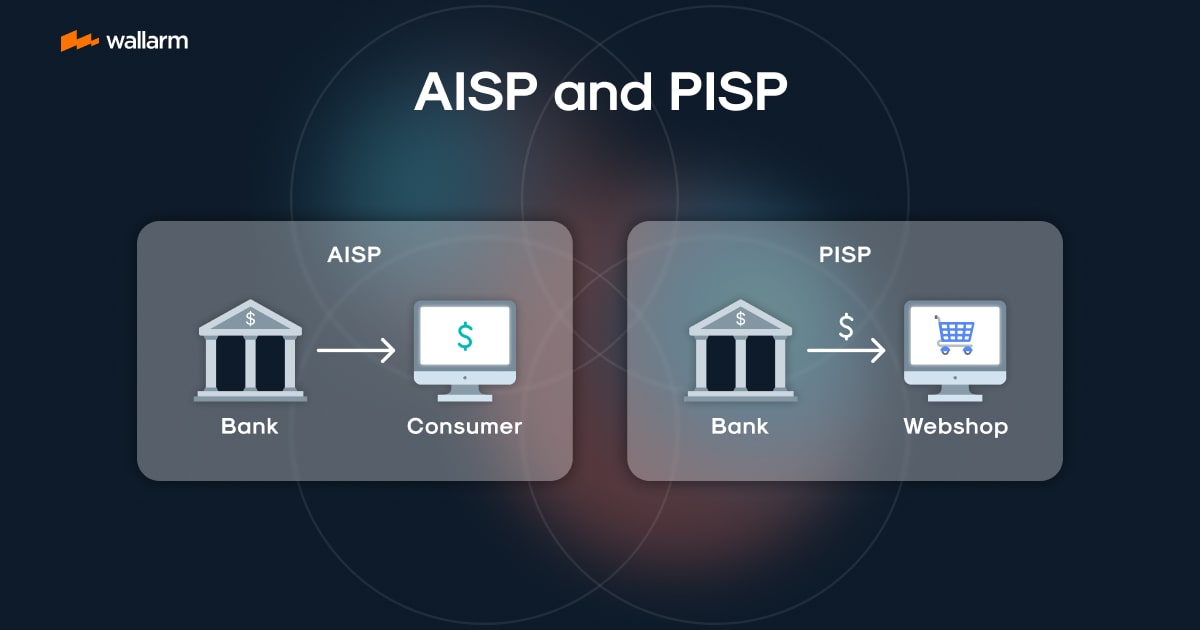

- Account & Transaction APIs: They grant TPPs access to account details and transactional data. Through this, TPPs can roll out services such as consolidated account views, budget management utilities, financial prediction tools, etc.

- Initiating Payment APIs: They permit TPPs to start payments for customers. Such APIs can be utilized for rolling out services like bill payment features, peer-to-peer money transfers, and e-commerce transactions, among others.

- Fund Verification APIs: They authorize third-party entities to ascertain the availability of sufficient funds in a client's account. Such APIs can lay the groundwork for services like credit appraisals and loan confirmations, etc.

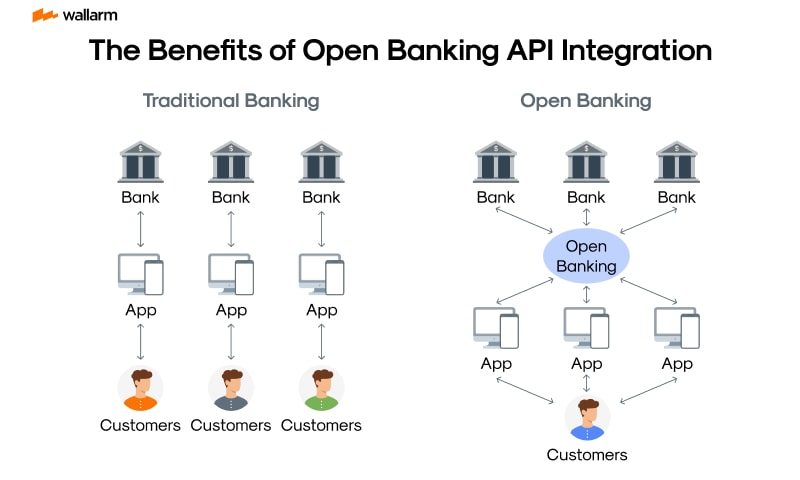

Contrasting Open Banking API & Traditional Banking

The Open Banking Application Programming Interface (API) serves as a digital mediator, fostering a conversation between distinct banking infrastructures and external apps. Its key purpose is to facilitate the safe and streamlined exchange of data. Here, an understanding of Open Banking API's operational intricacies, ingredients, and data distribution sequences will be presented.

Sub-divisions of Open Banking API:

Open Banking API's functionality hinges on an assortment of interconnected sub-divisions:

- Communication Channel (API Gateway): This primary touchpoint manages intercommunications from connected apps. Tasked with processing queries, it channels requests to the corresponding services as warranted.

- Data Safeguard (API Security): This element stands sentinel over all API-conveyed data, safeguarding it via data scrambling (encryption), tokenized validation (authentication), and access regulation (authorization).

- Developer Hub (API Developer Portal): Utilized by developers, this hub houses API pointers, details its capabilities, and provides the ''blueprints' (APIs) needed for app production.

- Usage Assessor (API Analytics): This component deciphers API application trends, supplies performance data, user interaction patterns, and highlights potential trouble areas.

Blueprint for Data Exchange:

Data distribution via Open Banking API is anchored by a methodical procedure:

- Access Consent (Authorization): Initially, the user needs to permit the external app to access their data. Primarily achieved via the OAuth 2.0 system, users are directed to their banking app or website to approve access.

- Access Proof (Token Generation): Post-access approval, the bank creates a one-of-a-kind access token for the third-party app, creating a digital 'key' for ensuing API interactions.

- Data Inquiry (Data Request): With its digital 'key', the third-party app can now query the API for specific data. This interaction includes the access token as proof of authorization.

- Data Procurement (Data Response): The bank's API gateway acknowledges the query, checks the access token's validity, and if approved, aids in retrieving the desired data.

- Data Delivery (Data Transfer): The obtained data is then securely conveyed to the third-party application through the API.

Procedural Protocols and Formats:

Open Banking API's preference leans towards REST (Representational State Transfer) procedures thanks to their straightforwardness and expandability. In terms of data representation, JSON (JavaScript Object Notation) is favored.

A short illustrative example of an API interaction to recover account details is:

In the instance provided, {accountId} would be substituted with the real account ID and {access_token} with the bank-granted access token. Application Programming Interfaces (APIs) in Open Banking operates as a secure digital tunnel, facilitating data transfer between banks and external applications. It depends on advanced web protocols and standards to underpin efficacious and impregnable data exchange, laying the groundwork for novel financial service inventions.

In a revolutionary move, the UK banking industry is undergoing dramatic change and innovation, thanks to the introduction of Open Banking API. This advanced software combination tool was born largely out of the shifting landscape in industry-specific regulations, the advent of cutting-edge technology, and consumers' growing demand for individualized banking experiences.

The conception of this avant-garde system was significantly influenced by the UK’s market regulation authority, known as CMA. Their ambition was to foster competition within the banking market and inspire the generation of inventive concepts. Consequently, in 2016, the CMA ruled that the top nine banking establishments in the UK, encompassing high-traffic banks like Barclays, Lloyds, and Santander, need to grant licenced financial technology (fintech) newcomers the ability to access their data repositories.

Further supporting this ruling, the European Union enforced the Second Payment Services Directive, also known as PSD2. This mandate stipulates that banks must open their customer data and payment systems to Third Party Providers (TPPs), assuming the customer provides their permission.

Consequently, UK banks quickly tapped into the potential of Open Banking API. This technological tool enables TPPs to process a client's financial information and execute transactions on their behalf, the effect being an uncomplicated financial performance. Additionally, to foster uniformity and maintain fluidity across all activities, banks have constructed fortified and secure APIs in alignment with the regulations set out by the OBIE (Open Banking Implementation Entity), a commission formed post CMA's directive.

By this dramatic shift in the banking ecosystem, customer control over personal financial data has greatly amplified, leading to a revolutionized banking experience. This facilitates customers to objectively review an array of financial tools and services delivered by several purveyors. It allows them to select suitable payment styles or manoeuvre their financial management through an all-in-one platform.

This shift opens doors to inventive business solutions embodied by fintech startups such as Yolt and Money Dashboard. By aggregating data across several bank accounts, these firms curate a comprehensive, unified panorama of a consumer’s financial situation.

With Open Banking API, the UK's traditional banking monopoly has been transformed to a liberal, inclusive model, as noticeable by the comparison chart below:

As more banking institutions and fintech companies collaborate with this agile infrastructure, the adaptability of Open Banking API is destined to escalate. It will further reshape customer interactions as service amalgamation leads to enhanced customization and distinctiveness in banking.

Optimizing Financial Processes Using Open Banking API

Open Banking API significantly modernizes the global financial landscape by revolutionizing how financial data is accessed and utilized. Let's dive into its practical applications:

Instance 1: Building Unique Customer Interfaces

The Open Banking API can be leveraged by finance companies to design powerful, customized services for their patrons. The API provides complete insights into financial transactions across various banking platforms, thus crafting an unparalleled end-user experience.

Instance 2: Enhanced Payment Gateways

Equipped with Open Banking API, individuals can perform banking transactions flaunting direct and card-less payment options. This alternative lowers transaction cost and delivers a speedy and safe method for funds transfer.

Instance 3: Tailoring Financial Advices

The Open Banking API is valuable when creating apps solely focused on streamlining an user's financial management. Armed with these apps, a user’s spending habits can be analyzed and specific suggestions for efficient money management can be given.

Instance 4: Expanding Third-Party Solutions

Open Banking API’s potential is not only confined to linking financial institutions. Other stakeholders, like third-party firms, can utilize the API access a user's transactional data and propose specialized financial services.

Instance 5: Accelerating Loan Approval Process

The role of Open Banking API is substantial in refining the loan application procedure. The API provides immediate access to the financial scenarios of applicants, accelerating the approval process and boosting the odds of obtaining loans.

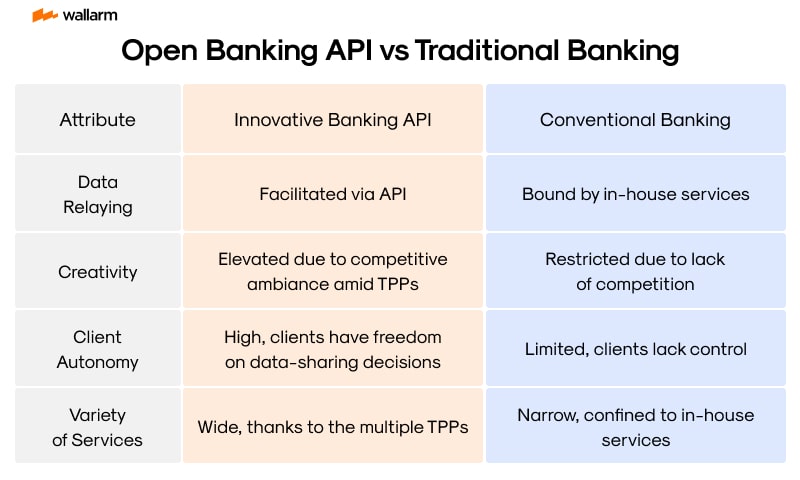

Contrasting Open Banking API and Conventional Banking Techniques

Utilizing Open Banking API: Python Example

The below Python code demonstrates how account details of a user can be accessed using the Open Banking API.

The code initiates by importing the Python requests module which is then used for making HTTP requests. Headers carry the access token and requested data type for the API. An HTTP GET request to the Open Banking API URL fetches desired data, thus exemplifying how Open Banking API can be used to elevate financial processes and personalized services.

Defining Operational Goals

To choose an Open Banking API tailored to your distinct requirements, start by comprehending what those needs are. Gain an understanding of what aspects such as payment initiation, fund validation or account information services your Open Banking require. The API must correlate with your business plan and operational specifications.

Analysing API's Efficiency

API efficiency can greatly influence user satisfaction and overall system productivity. Thus, check for API's latency since a high latency can be detrimental. Components such as response velocity, rate restrictions and operational duration should be analysed critically. Tools like SoapUI or Postman could be beneficial for assessing these parameters.

Safeguarding Confidentiality and Adherence to Policies

Maintaining data privacy is of utmost importance in banking. The chosen API needs to fulfill strict security norms to safeguard customer data. Opt for APIs implementing secure protocols like OAuth2 along with providing encryption features. The API should also meet specifications imposed by regulatory entities such as the EU's PSD2 and the UK Open Banking Standard.

Easy Accessibility and Support

Effective documentation simplifies the integration process drastically. It should offer an easy understanding of API usage, consisting detailed path-descriptions and helping with extensive sample codes. Additionally, evaluate the extent of assistance offered by the API provider. This may include round the clock help or a dedicated account handler for aid.

Cost Evaluation

Examination of service cost forms an integral part of the selection process. Compare pay-as-you-go models with fixed annual or monthly fees. Estimate your API usage frequency and take your budget constraints into consideration when deciding which plan meets your needs best.

Compatibility

Ensuring the API's adaptability with your pre-existing software and systems is important. This includes support for universal data formats such as XML and JSON and utilizing standard HTTP operations. A compatible API can minimize time and expense involved in integration.

Sustainability

As your organization expands, your API requirements will scale too. Hence, select an API that can handle this growth. Analyze aspects like rate limitations and the API's capability to manage amplified traffic while maintaining optimum performance levels.

Assessing Provider Credibility

The credibility of the API provider also merits consideration. Investigate their history, client testimonials, and successful use cases. Trustworthy providers will likely deliver dependable and superior quality APIs.

Deploying AI & ML for Efficiency Improvement in Transparent Financial Tech Procedures

Employing artificial intelligence (AI) and machine learning (ML) in fintech protocols significantly boosts their performance capacity. The prowess of AI lies in deciphering and understanding inferred patterns in individual transactions, thereafter offering tailored monetary guidance. Concurrently, ML amplifies cyber-protection by detecting anomalous behaviors, thereby fortifying safety features in currency transfers.

Innovative Tactics in Customer-Driven Banking

Customer-driven banking's less restrictive attributes have triggered exceptional expansion within the finance sector. Emerging fintech ventures leverage customer-accessible financial modules to develop imaginative solutions that vie with traditional banking processes. These cutting-edge solutions incorporate efficient loaning platforms and digital money trade facilities.

The emergence of customer-centric banking schemes has given birth to flexible "Bank-as-a-Service" (BaaS) prototypes. These systems offer customers an ample suite of banking tools such as capital management, money transfers, and virtual spending procedures. Infallible API collaboration expedites this transition from classic to sophisticated banking methodologies, increasing adroitness and fiscal productivity.

IoT Evolution Coupled with Customer-Driven Banking

The marriage of Internet of Things (IoT) and customer-driven banking denotes a dramatic drift in the banking spectrum. Melding IoT-enabled devices like sophisticated home appliances and advanced wearable technology with customer-accessible financial setups, novel facilities can be launched.

Imagine an IoT-enabled smart refrigerator integrated with customer-driven banking platforms, designed to restock groceries and implement automatic payments from connected bank accounts. In a similar vein, associating wearable tech with a customer-driven banking system could transform hands-off financial transactions.

Cultural Influence of Customer-Driven Banking

Triggered initially in the UK, customer-driven banking now influences international banking operations. The European Union's compliance with Payment Services Directive 2 (PSD2) mandates banks disclose client data to accredited third-party organizations. Countries such as Australia and Canada are navigating their journey towards adopting customer-driven banking processes.

Global acceptance of customer-driven banking could generate a synchronized international money transfer model, propounding a uniform financial framework.

Fortifying Safeguarding Practices in Customer-Driven Banking Procedures

The global spread of customer-driven banking demands robust security architectures. Integrating biometric safety elements like finger scanning mechanisms and face identity verification systems could enhance existing security measures. Moreover, the addition of digital ledger methodology, blockchain, might offer a safeguarded and transparent arena for financial interactions.

Thus, it becomes critical for all stakeholders - traditional banking sectors, burgeoning fintech enterprises, and governing bodies - to collaboratively ensure secure, and efficient functioning of customer-driven banking procedures.

Open Banking API has revolutionized the banking sector, providing a platform for innovation, competition, and customization. It has opened up a world of opportunities for financial institutions, fintech companies, and consumers alike, enabling them to create and access a wide range of personalized financial services.

Embracing Customization with Open Banking API

Open Banking API allows financial institutions to share their data securely with authorized third-party providers. This data sharing capability enables the development of new financial services and applications that can be tailored to the specific needs of individual consumers.

For instance, a third-party provider could use the data shared via an Open Banking API to develop a personal finance management app that provides consumers with a comprehensive view of their financial situation, including their bank account balances, credit card transactions, and investment portfolio. This level of customization was previously unimaginable in the traditional banking sector.

The Role of Open Banking API in Enhancing Security

Open Banking API not only facilitates customization but also enhances the security of financial transactions. It does this by implementing stringent security protocols and standards, such as OAuth 2.0 for authentication and authorization, and Transport Layer Security (TLS) for data encryption.

Moreover, Open Banking API mandates the use of strong customer authentication (SCA), which requires at least two independent elements out of something the customer knows, something the customer has, and something the customer is. This multi-factor authentication significantly reduces the risk of fraud.

Wallarm API Attack Surface Management (AASM)

While Open Banking API has numerous benefits, it also presents new security challenges. The increased data sharing and interconnectivity can potentially expose financial institutions to cyber threats. This is where Wallarm API Attack Surface Management (AASM) comes into play.

Wallarm AASM is an agentless detection solution specifically designed for the API ecosystem. It helps financial institutions discover external hosts with their APIs, identify missing WAF/WAAP solutions, discover vulnerabilities, and mitigate API leaks.

By integrating Wallarm AASM into their security infrastructure, financial institutions can effectively manage their API attack surface and protect their data from potential cyber threats.

The Power of Open Banking API and Wallarm AASM

The combination of Open Banking API and Wallarm AASM provides a powerful solution for financial institutions. Open Banking API enables them to innovate and customize their services, while Wallarm AASM ensures that they can do so securely.

To experience the power of this combination, financial institutions are encouraged to try Wallarm AASM for free at https://www.wallarm.com/product/aasm-sign-up?internal_utm_source=whats. This trial will provide them with firsthand experience of how Wallarm AASM can enhance their security infrastructure and protect their data in the Open Banking API ecosystem.

In conclusion, Open Banking API is a game-changer in the banking sector. It provides a platform for innovation, competition, and customization, and with the right security measures in place, such as Wallarm AASM, it can also enhance the security of financial transactions. Therefore, financial institutions should embrace the customization offered by Open Banking API and equip themselves with robust security solutions like Wallarm AASM to navigate the new horizon of banking securely and confidently.

FAQ

References

Subscribe for the latest news

.png "AWS with Wallarm")