Banking as a Service (BaaS): What It Is + Examples

Prominent strides of technology in the banking sector have sharply pivoted towards the path-breaking capabilities of BaaS (Banking as a Service) API. Acting as a conduit for standalone programmers, it can harness essential banking services and weave them into a more tech-driven operational layout that spans across a myriad of applications and platforms.

Framework Ins and Outs of BaaS API

A suite of ground rules and tools forms the base structure of BaaS API, aiming to support the interaction of programmers with established banking mechanisms. BaaS API, being an open window to the bank's operational core, also fosters a potent conversation with the outer universal interface. Programmers can tap into this robust and universally relevant strategy to access underlying banking dimensions like account management, disbursements, and fund transfers.

In line with RESTful standards, BaaS API incorporates prevalent HTTP methods, such as GET, POST, PUT, and DELETE. This adherence enables programmers to intertwine the API with their applications, notwithstanding the programming dialect used.

BaaS API: Navigating Through its Complex Service Disposition

BaaS API's working model resides deep within an entwined network of comprehensive services and sophisticated software. This nexus primarily consists of archetypal bank infrastructure, auxiliary programs, and the BaaS API itself. The primal banking regimen structures the principal connectivity point, driving conventional banking services. BaaS API, in its capacity, smoothens the incorporation of these services with external applications.

Applications tapped into the BaaS API can range from mobile banking apps to web-centric business podiums. Embedding banking services into these platforms fosters an uninterrupted user experience.

Benchmarked Comparison: BaaS API Layout Vs Standard Banking

Traditional banking works within its stringent boundaries, providing services through an internal mechanism that prioritizes security but limits flexibility and innovation. In contrast, BaaS API serves as a permeable system, granting external programmers to harness and implement banking services. This tactic safeguards the system's integrity while promoting substantial flexibility and creativity.

Tapping Into the Potential of BaaS API

Emerging BaaS API capabilities can yield transformative outcomes for the financial sector. It allows traditional banks to dismantle geographical barriers, enabling customer interactions from afar. Additionally, it supports developers in crafting more comprehensive applications, infusing banking operations to ensure smooth customer journeys.

An instance of this is how mobile applications can harness BaaS API to integrate banking functions and services, allowing consumers to process payments within the app itself. Such a strategy not only enriches the user experience but also opens new revenue channels for banking organizations.

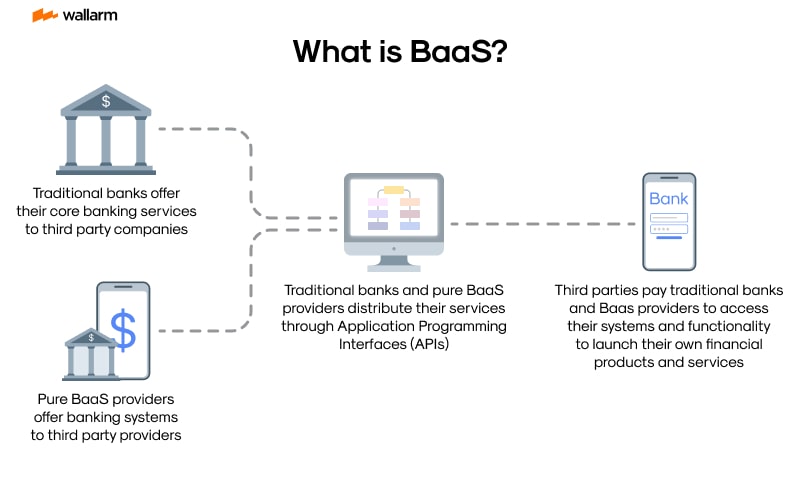

Banking-as-a-Service (BaaS) API is an innovative mechanism enabling third-party developers to liaise and merge banking functionalities to their software platforms. This transformative tech-oriented approach aids in enhancing the fiscal domain via a smooth, impenetrable, and competent route to render banking amenities to clientele.

BaaS API's Structural Composition

BaaS API operates based on a microservices framework—a design principle where multifaceted applications are crafted as a conglomerate of several petite services, all functioning independently and communicating through primal mechanisms. This setup promotes the swift, dependable, and scalable dispersion of intricate applications.

The structure of the BaaS API encompasses several subcomponents, which are:

- Identification Service: This constituent certifies that only valid users have the liberty to access the banking functionalities. It employs measures such as OAuth2 and OpenID Connect for assuring barricaded access to the API.

- Account Administration Service: This functionality deals with all tasks tied to the user's financial account, for instance, balance verifications, past transactions' review, and capital reallocations.

- Monetary Transactions Service: This element looks after all payment-directed procedures like bill settlements, capital movements, and automated deductions.

- Client Information Service: This functionality supervises all client-centric data like personal facts, means of communication, and account predilections.

The Functioning of BaaS API

The BaaS API operates by exhibiting a set of RESTful points that third-party developers can utilize to interlock with the banking amenities. These points are usually structured around the financial resources, embodying accounts, transactions, and payments.

For instance, a software developer might engage the subsequent HTTP methods to liaise with the account resource:

- GET /accounts: Recover an inventory of all accounts

- GET /accounts/{id}: Recover the specifications of a distinguished account

- POST /accounts: Form a novel account

- PUT /accounts/{id}: Ameliorate the specifications of a distinguished account

- DELETE /accounts/{id}: Eradicate a distinguished account

Each of these methods equates to a peculiar task that can be enacted on the account resource.

The Implications of BaaS API

Utilizing the BaaS API offers several essential advantages to the two primary users—banks and third-party developers. For banking institutions, it provides a passage to broaden their services reach, surge their operational competence, and maintain their competitive edge in the digitization era.

For developers, it offers a normalized, secured, and proficient route to merge banking functionalities into their software platforms. However, utilizing the BaaS API comes with some intricate complications—it necessitates substantial endowment in infrastructure, digital security, and adherence to regulations.

Moreover, it demands comprehensive knowledge of both fiscal domain and tech-oriented realm, which may seem an overwhelming task for many organizations. Nonetheless, despite such hurdles, the BaaS API is progressively turning into an essential element of the contemporary fiscal arena.

Evaluating BaaS API: Understanding the Obstacles and Prospects

BaaS API Roadblocks

Navigating Legal Frameworks

A significant hurdle in incorporating BaaS API into traditional banking structures is the intricate web of banking laws that banks must abide by. These regulations differ drastically across geographical regions, making the process of ensuring full compliance even more challenging when integrating BaaS API.

Safeguarding Data

On account of rising online threats, defending client data has become an uphill battle for banks. Incorporating BaaS API into banking systems could potentially expose clients' sensitive information to cyber attacks. Hence, fortifying security protocols to prevent such data breaches poses a major challenge.

Adapting Current Technological Frameworks

A pressing issue for older banks is the possible incompatibility of BaaS API with their existing technology frameworks. The upgradation process to create a seamless integration of these new technologies can be lengthy and financially hefty.

Convincing Clientele

Despite the manifold advantages of BaaS API, persuading clients to place their trust in this nascent technology remains an arduous struggle. Apprehensions about digital banking solutions and data protection are prevalent, making the move toward digital banking a hesitant one for many customers.

Prospects Offered by BaaS API

Refining Customer Endeavours

BaaS API equips banks with the capability to deliver custom-tailored, smooth banking experiences. By unifying a gamut of services under one platform, customers can effortlessly access a myriad of banking facilities.

Operational Expenditure Reduction

A notable benefit of employing BaaS API is a substantial decrease in running costs. The system enables the automation of several banking tasks, eradicating the necessity of human intervention and resulting in significant savings.

Unexplored Revenue Avenues

BaaS API reveals untapped revenue sources. Banks may grant access to their API to independent developers who could create ingenious banking applications. This approach not only expands the customer reach of the bank but also spearheads additional revenue generation.

Driving Innovation and Nimbleness

BaaS API empowers banks to readily adjust to shifting market tendencies and customer inclinations. This technology propels banks' innovation capabilities, allowing them to roll out new services and stay abreast of the competition.

Utilization of Banking-as-a-Service (BaaS) Application Programming Interfaces (APIs) has ushered a transformative era within the finance sphere. The fundamental implications of this technology reach far beyond merely rendering banking activities efficient - it bolsters the customer journey and leaves an indelible mark on the industry.

1. Fluidity in Operations

Employing BaaS APIs effectively turbocharges banking functions that were traditionally manual and consequently, laden with inaccuracies and inefficiencies. A classic example is account initiation - an erstwhile lengthy procedure now expertly trimmed down to mere minutes with BaaS API. Analogously, financial transactions once marred by delays, can be seamlessly accomplished in mere seconds, cutting down substantial operational expense for both banks and other fiscal associations.

2. Customer Expereince Amplified

BaaS APIs have an uncanny knack for augmenting the customer journey. This technological marvel empowers banks to curate personalized services for their patrons. From verifying their account status, executing fund transfers to loan applications - all these facilities can be summoned on mobile gadgets. This element of convenience has a side benefit - increased user activity. Additionally, the accessibility of banking services round-the-clock is another advantage, allowing customers to control their banking needs at their leisure and space.

3. A Catalyst for Innovation

The BaaS API platform is a breeding ground for inventive applications. Novel apps and services designed by third-party developers find seamless integration within banking systems, enhancing their functionality holistically. Examples include crating apps that assist customers in sustaining their financial health, expenditure tracking, and even dabbling in the stock market. The end product is a robust and inclusive financial solution for customers, thanks to the integration capabilities of BaaS APIs.

4. Encouraging Fiscal Inclusion

BaaS APIs are an effective tool in bridging the banking gap for unbanked and underbanked communities. Using this technology as a conduit, banks can extend their outreach to these demographics, paving way for comprehensive financial services. This optimistic trend is a leap towards financial inclusion and a premise for potential new segments for banking organizations.

Amplifying Web-Based Banking Procedures Using BaaS API Resources

The epoch we live in witnesses the evolution of banking approaches largely steered by tech breakthroughs. The BaaS API toolkit stands as a prominent navigational tool amidst this dynamic whirlpool. Further, BaaS API extends its reach, navigating beyond the conventional borders of banking operations to touch down on the realms of joint digital applications.

The amalgamating crucial banking functions with mobile tech gains significant relevance in the current mobile-centric timeline. The BaaS API works as an effective binding prop, smoothening the synthesis of banking and mobile tech. The upshot is a streamlined internet-banking route that boosts client satisfaction.

BaaS API’s Role: Actuating Banking Digital Transformation

Beyond just uplifting customer experiences, BaaS API presents itself as the key catalyst activating seismic digital shifts within banking circles. This disruptive invention carves efficiencies by invoking a cutting-edge tech approach into regular banking chores.

An illustrative example is the conventional loan sanctioning method. Automating this vital banking function can be enriched through the BaaS API. By melding it with a loan origination protocol, the API eradicates mistakes stemming from human involvement and fast-tracks the loan disbursement process.

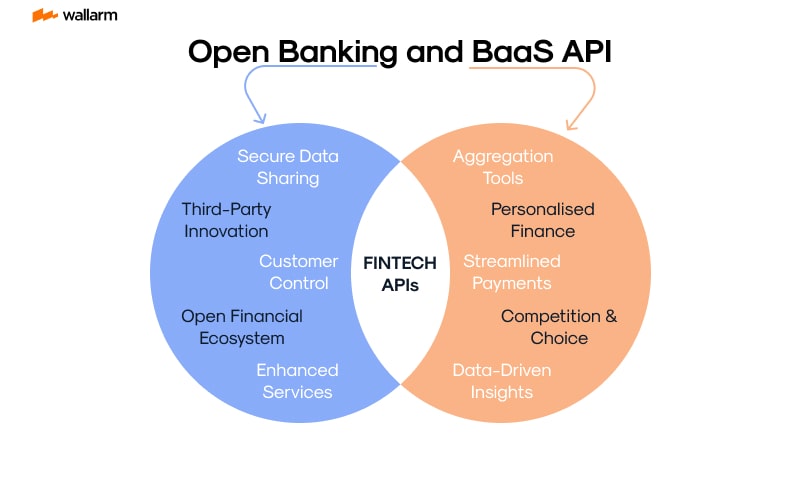

Revolutionizing Conventional Banking Obstacles with BaaS API and Open Banking

Open banking endorses a transition from conventional in-house banking towards a strategy of exchanging data with third-party services. BaaS API becomes the pivotal player in steering this information decentralization process.

A relevant instance includes a bank utilizing a BaaS API for transmitting client information to an independent financial enterprise. This receiving entity can then repurpose the data to structure personalized fiscal offerings, thereby germinating a value-added, customer-centric banking environment.

Promoting Financial Equality through BaaS API Application

Being a significant prop in broadening banking reach, BaaS API champions the move towards inclusivity in locales furnished with digital tech. By shaping a neatly ordered online banking system, BaaS API nurtures diversity within the financial sector.

Banks that apply BaaS API to render mobile banking functionalities in remote areas are essentially fueling financial equality. This action ensures that communities typically lagging in conventional banking access can avail banking facilities.

Simplifying Regulatory Compliance with BaaS API Implementation

Adhering to banking regulations can entail intricate procedures. As a solution, BaaS API operates as an expeditor simplifying this maze through automation.

To cite an example, automating Anti-Money Laundering (AML) screenings becomes achievable through BaaS API. The unification of the API with AML software enables real-time suspicious activity tracking, thus permitting banks to easily comply with AML regulations.

SolarisBank: Trailblazing BaaS API

Opening the discussion with SolarisBank, a notable fintech entity based in Germany. Synonymous with revolutionary BaaS solutions, SolarisBank has mastered the utilization of APIs to orchestrate an array of banking amenities. Their business strategy is deeply rooted in the principle of 'API-first', allowing corporations to assimilate banking services within their application landscape, hence achieving an uninterrupted end-user experience.

By conferring services like digital banking, card facilitations, KYC procedures, monetary transactions, and lending operations under one API roof, SolarisBank has removed them from the onus of establishing banks for affording banking services. An apt illustration would be Kontist, a banking application designed for freelancers and self-employed society, which delivers tailor-made banking solutions with the help of SolarisBank's APIs.

Starling Bank: Iconic BaaS API Journey

Moving to Starling Bank, a prestigious challenger bank hailing from the UK. It has made its mark in the BaaS API sector by offering access to sundry banking chores such as managing accounts, transactions, and controlling card operations. Their API platform has instigated enterprises to cultivate state-of-the-art financial commodities and services based on Starling's formidable banking structure.

Point in case is Flux, an avant-garde platform for digital receipt dispensation and reward settlement, harnesses Starling Bank's API to automate digital receipt transfer into customers' banking interfaces. This not just flourishes customer interaction but also grants Flux a renewed medium to connect with customers.

BBVA: BaaS API for Borderless Reach

Next in line is BBVA, a globally recognized Spanish banking percussion, that has adopted BaaS API for proliferating its reach across borders. Their collaborative Open Platform is studded with a group of APIs, enabling corporate entities to homogenize banking solutions into their application workflow. This strategic step has permitted BBVA to launch its banking amenities in territories sans physical existence.

Noteworthy collaboration in this regard is BBVA's alliance with Uber in Mexico. The latter employs BBVA's Open Platform to extend an offer of digital banking account as well as a debit card to its patrons including drivers and couriers. This marketing finesse has not just widened BBVA's consumer pool but also facilitated Uber's associates with monetary services, for some it being their maiden experience.

Fidor Bank: BaaS API for Inclusive Banking

Finally, we have Fidor Bank, a pacesetting digital bank from Germany, that has capitalized on BaaS API to model a banking environment driven by community needs. Their API offers authorities to outside developers to invent applications that incorporate Fidor's banking resolutions, culminating into an all-encompassing spectrum of monetary goods and services that align with Fidor's community prerequisites.

An example to illuminate this would be Fidor's collaboration with Ripple, a forward-thinking digital remission protocol. The service generated on Fidor's API architecture enables patrons to execute international funds transfer at minimal cost. This unique offering not just furnishes added advantage to Fidor's customers but also distinguishes it from conventional banks.

Elevating Security for BaaS API: Introducing Protective Actions

The multifaceted environment of BaaS API consistently encounters risks linked to unauthorized modifications and data breaches. A comprehensive security strategy is crucial to mitigate such threats.

Deploying Robust Encryption for Secure Data Activities

By leveraging encryption technology, data within BaaS APIs are cloaked, preventing undesired data interference during its transfer or storage phase. Strengthen this digital safeguard by implementing trusted encryption techniques, such as SSL or TLS, for data transfer, and AES for safekeeping during storage.

Amplifying Access Control Strategies with Authorizations

Access scrutinizing protocols, integrated into the authorization routine, thoroughly examine each user or system without exception, attempting to interact with the BaaS API. Once validated, the authorization structure defines the allowed tasks for each user or system. Integrate comprehensive solutions like OpenID Connect or OAuth 2.0, blending tough authentication and authorization codes, that are central in maintaining a solid security framework.

Incorporating Usage Rate Limiting Procedures to Shield BaaS API

Limits on the volume of requests a user or system can make within a given timespan serve as a protective barrier against mass onslaughts such as DoS by averting API overloading and subsequent potential misuse.

Regular Revamp of Security Approaches: Current Necessity

Guarding BaaS APIs is a fluid process that demands adjustment and response to evolving threats.

Periodic Security Review for Enhanced Safeguarding

Timed inspections of security at fixed intervals facilitate identification of potential weak points and ensure alignment with critical security protocols. These checks should thoroughly review all aspects of the BaaS API.

Prioritizing Security in the Design Phase of BaaS API

Security needs to be acknowledged as an essential component from the initial stages of BaaS API creation, mirroring the 'security by design' principle and involving detailed embedding of security elements during all periods of the API's lifecycle.

Persistent Monitoring and Swift Threat Resolution

Real-time monitoring of all BaaS API transactions alerts to potential insecurity, and a responsive threat management approach essential for immediate threat neutralization, thereby mitigating possible damage.

Practical Example: Lessons from Bank X’s Security Strategies

Bank X employs an exemplary approach to BaaS API security that serves as a useful reference in today's digital era. Bank X's multi-layered strategy contains:

Bank X applies stringent encryption, leveraging SSL/TLS for data transfer and AES for data storage. They regulate access to their BaaS API using OAuth 2.0, controlling permissions for different operations.

Bank X averts large-scale attacks and possible API misuse by effectively using rate limiting. Routine security evaluations are conducted to demand strict compliance and reveal potential points of weakness. Upholding the 'security by design' principle, Bank X integrates protective measures at each phase of the API process.

Bank X maintains a mechanism for rapid identification and rectification of security gaps, made possible by continuous monitoring of API transactions and a proactive incident management strategy. The comprehensive defensive plan of Bank X serves as a sturdy guard against increasing digital threats.

The Evolutionary Path of BaaS API

The digital realm features BaaS API as a progressive power, eager to redefine customary banking protocols. Physical banking methods and manual monetary transactions face replacement, supplanted by the dawn of a robotized, digital, and customer-centric financial world. This migration is primarily driven by BaaS API, recalibrating banking services into a mode that is elastic, expandable, and cost-effective.

The forthcoming banking scenario will exhibit an expansive inclusion of BaaS API. This interface will undertake the delivery of a vast array of amenities, from rudimentary banking mechanics such as account surveillance and remittance to complex procedures like credit provision and capital administration. This mutation will not only revamp customer engagement but also realizes untapped lucrative trajectories for banking institutions.

The Advent of Transparent Banking

Transparent Banking, an emerging inclination, stands ready to wield a substantial sway on the upcoming direction of the BaaS API. This methodology empowers banks and alternative finance establishments to disseminate their data through APIs. Consequently, this gives independent creators the opportunity to derive applications and services revolving around these economic entities, thus augmenting creativity and rivalry.

As transparent banking gains ground, the spectrum of APIs rendered by banks is set to grow exponentially. The fresh set of interfaces will work as a stimulant for standalone developers to generate a myriad of services from personal finance administration tools to channels of remittance, thus increasing customer engagement.

The Fusion of AI and Machine Learning

AI and Machine Learning will impart a deep-seated effect on the future trajectory of BaaS API. Utilizing these innovations, banks can meticulously analyze extensive datasets, discern patterns, and envisage future possibilities. This affords them the capability to deliver individualized and efficient services curated to individual customer needs.

For example, leveraging AI and Machine Learning can assist in analyzing a client's expenditure manners and deliver customized financial advice. Concurrently, these technologies can be used in real-time to identify and alarm abnormal transactions, thereby bolstering the security infrastructure of banking procedures.

Proactive Steps towards Superior Security

The ascending usage of BaaS API demands the implementation of robust security measures. Banking institutions must ensure their APIs are immune to digital threats, as any violation could lead to massive fiscal damage and tarnish their established repute.

Answering this call is Wallarm API Attack Surface Management (AASM), a solution sans the need for an agent. Wallarm AASM is skilled in discovery and alleviation of vulnerabilities within the API ecosystem. It's conscientiously designed to reveal external hosts and their APIs, identify missing WAF/WAAP solutions, detect security discrepancies and prevent API leaks.

The inclusion of Wallarm AASM enables banks to shield their APIs robustly - equipping them to face the rigorous challenges lying ahead. For a proof of concept of the benefits of Wallarm AASM, banks can avail of the free trial here: https://www.wallarm.com/product/aasm-sign-up?internal_utm_source=whats.

Undoubtedly, the forthcoming journey for BaaS API looks bright and striking, characterized by escalated presence of APIs, transparent banking, the amalgamation of AI and ML, and proactive security initiatives. For banking institutions, keeping in step with these shifts and leveraging them to their edge is an essential mandate.

FAQ

References

Subscribe for the latest news

.png "AWS with Wallarm")